An article written by Gabriel Li (Vice President, Legal at Kredivo Group Limited) and Dr Jeremy Loh (Genesis Alternative Ventures) explains liquidation preference. Published by the Singapore Law Watch.

If you’re in the process of seeking equity financing or have done so previously, you’ve likely encountered the concept of “liquidation preference.” While online searches yield numerous articles providing a general overview, they often lack region-specific insights, particularly for founders seeking funding for a Singapore private limited company. This article offers a comprehensive introduction to “liquidation preference” within the Southeast Asia context, along with practical negotiation advice.

Tough, challenging, economic headwinds, cautious optimism, interest rate hikes, downrounds, pay-to-play, layoffs – all these were words that startup entrepreneurs and venture investors became familiar with 2023. However, the year also saw several noteworthy developments that had a lasting impact on the venture capital landscape. We will address them in this quarter’s House View.

AI Ascending

2023 was a defining year for the Artificial Intelligence (AI) industry. AI became increasingly integrated into various industries, including healthcare, finance, manufacturing, and retail. Developments in machine learning, natural language processing, computer vision, and robotics were at the forefront of AI advancements. These technologies were driving innovation across sectors. Businesses leveraged AI to improve efficiency, customer experiences, and decision-making processes. Large tech companies continued to acquire AI startups to enhance their AI capabilities and expand their market presence. Microsoft became a leader in AI adoption with close integration of ChatGPT into its Bing search engine since announcing a $10 billion investment in OpenAI, the creator of the ChatGPT chatbot. What is exciting is the combination of the power of large language models (LLMs) with data in the Microsoft apps to turn words into the most powerful productivity tool on the planet. But as AI adoption grew, there was also a growing focus on ethics and regulations surrounding AI applications, particularly in areas like data privacy and algorithmic bias.

Silicon Valley Bank Collapse

One of the most notable events of 2023 was the sudden collapse of Silicon Valley Bank in March, a venerable institution that had long been synonymous with the technology and innovation hub of California. Its downfall sent shockwaves through the startup ecosystem, serving as a stark reminder of the fragility that can underlie even the most established financial institutions. In the aftermath of SVB’s failure, startups and venture capital funds faced not only the practical challenges of disrupted financial operations but also the psychological impact of shattered trust in financial institutions. This event served as a critical lesson in risk management and diversification, reinforcing the need for resilience and adaptability in the ever-evolving landscape of the startup and venture capital world. It also highlighted the importance of contingency planning and the necessity of spreading financial risks across multiple trusted partners to safeguard the interests of all stakeholders.

End of IPO Ice Age?

The IPO market remained frozen throughout 2023, save for a few iconic listings like Arm, Instacart, and Klaviyo, depriving startups of a traditional exit strategy and forcing them to reassess their growth trajectories. Courier startup J&T Global Express, which launched in Indonesia before expanding across Southeast Asia and China was valued at $13 billion in its Hong Kong IPO, below its last private round valuation of $20 billion as reported. Singapore’s first SPAC, VTAC, listed in January 2022 and backed by Vertex Venture Holdings, the venture capital arm of Singapore’s sovereign wealth fund, Temasek Holdings. VTAC merged with Asia’s live streaming app 17LIVE to take the startup public on Singapore’s stock exchange in December 2023.

What could be the catalyst that rekindles the interest in tech startup IPOs? First and foremost, a resurgence of confidence in market stability is essential. Renewed assurance that market volatility could be normalizing may set the stage for increased IPO activity. Furthermore, decisions made by the US Federal Reserve and other central banks concerning interest rates will wield considerable influence. These decisions ripple through the technology sector, impacting future cash flows of companies, driving valuation rebounds, and shaping investor sentiment. The current challenging capital market conditions present an opportune moment to lay the groundwork for an IPO, especially considering that the preparation process typically spans 12 to 18 months. Commencing preparations today positions companies to be fully prepared when favorable market conditions eventually return. On the 2024 IPO pipeline watchlist are some exciting candidates, including OpenAI which saw a leadership drama cutting its valuation down to $50B, Stripe – the Fintech payment darling that played a key role in disrupting the payments world with an estimated $50B valuation and Canva, the Adobe competitor with a potential $10B valuation.

From Setbacks to Comebacks

As we navigated the year, venture capital funds found themselves closing the books on a tough and transformative period. VC deals, exits, and fundraising all experienced a dramatic downturn, challenging the industry’s resilience and adaptability.

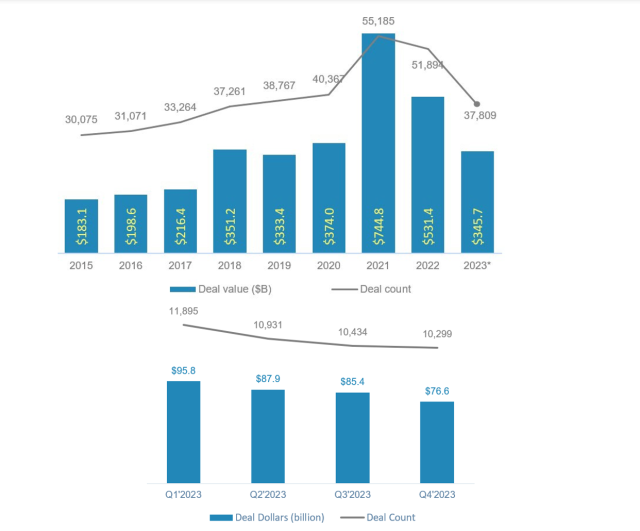

Global VC funding plummeted to approximately $345 billion, a substantial decline from the robust $531 billion recorded in 2022. This was reflected in both declining global VC deal count and dollars as illustrated below.

Source: PitchBook Q4 2023 Global Venture First Look

Southeast Asia observed a near identical trend. According to DealStreet Asia’s Singapore Venture Funding Landscape 2023 report, the region registered a 30% year-on-year decline in deal volume in 2023 (9 months) with total deal value down by 50%. While Singapore continues to be the region’s top tech investment destination (64% of total deal volume), deal value (-49%) and deal volume (-21%) both registered declines in 2023. Seen in context however, funding activity has reverted to levels last seen in 2019 which is an encouraging sign given that “the subsequent funding surge during 2021-2022 was an anomaly fuelled by a global liquidity glut”. Further, we note that “Seed to Series B” deals garnered a larger share in 2023 “indicating a growing investor preference for moving upstream”.

Facing a capital crunch and a prolonged fundraising runway that typically stalled on the topic of valuation, startups have had to trim their operations to achieve financial sustainability. Those that were able to achieve this newfound cashflow breakeven were in a unique position to capitalize on a changing business landscape. Founders started to experiment with marketing strategies that increase ROI (return on investment) – for example, optimizing marketing spend by adjusting social media campaigns to reduce burn and drive outcomes, reducing product SKUs, negotiating and extending payment terms extending working capital cycles. With healthy cash reserves in bank accounts, these lean and financially positive startups were not just weathering the challenging market conditions but actively seeking opportunities to expand their influence and market share.

Founders also recognized that a tumultuous year had created fertile ground for strategic acquisitions and talent acquisition through acqui-hiring. One notable example was turnaround fund Turn Capital acquisition of Flash Coffee’s business in Thailand. This strategic move aimed at revitalising Flash’s coffee business and aims to open over 100 new stores within the next two years. Another compelling instance unfolded in the acquisition of Loom, a video messaging startup that had once achieved unicorn status. Collaborative software giant Atlassian recognized the potential and value in Loom and acquired the San Francisco-based startup for a substantial $975 million. Notably, Loom had recently raised $130 million in a Series C funding round in May 2021, at a valuation of $1.5 billion. Atlassian’s acquisition represented a strategic move to leverage Loom’s capabilities, and despite the 35% decline in valuation from the previous round, it underlined the significance of acquiring talent and technology to drive future growth in the rapidly evolving landscape of tech startups.

In the current global startup landscape, a positive and healthy recalibration period is underway, exemplified by success stories like Lenskart’s recent achievement. Securing a substantial $500 million investment from the Abu Dhabi Investment Authority at a solid $4.5 billion valuation, Lenskart’s remarkable journey showcases the potential for startups to thrive when pursuing profitability and strategic excellence. With a network spanning 2000 stores across India, Southeast Asia, and the Middle East, Lenskart not only highlights its impressive scale but also underscores its claim to profitability—a rare feat in the startup world. This milestone serves as a valuable lesson for all emerging companies, emphasizing the need to reevaluate their strategies. Startups are now encouraged to shift their focus towards profitability, exercise prudent expense management, and prioritize establishing a strong market position. However, Lenskart was not alone in its impressive feats. Other startups also closed spectacular funding rounds in the final weeks of 2023, solidifying the industry’s positive momentum. Klook, a trailblazer in the travel technology sector, secured an impressive $210 million in Series E+ funding. Simultaneously, Silicon Box, a key player in the semiconductor arena, raised a significant $200 million in Series B funding.

Fundraising Gains Momentum

Venture funds witnessed a decline in fundraising, reflecting a stark contrast to the previous year’s numbers. VC firms managed to collect only $161 billion, a considerable drop from the impressive $307 billion raised in the preceding year. Notably, New Enterprise Associates (NEA) stood out as a fundraising leader, securing slightly over $6.2 billion for two new funds, and with NEA announcing its first Indonesia investment into Gravel, an Indonesia-based construction tech startup raising $14m Series A to extend its capacity to help anyone build, renovate, and repair living, working, and recreational spaces efficiently by using technology to connect customers to not only qualified construction workers, but also tools, building materials, and experts. Meanwhile, Bain Capital Ventures, a San Francisco-based multi-stage venture capital firm, successfully closed two funds, amassing a total of $1.9 billion in commitments.

Vertex Ventures also made headlines by finalizing Fund V with $541 million, adding to the growing momentum of venture capital in the region. Meanwhile, Singapore-based Northstar Group achieved a significant milestone by completing the fundraising for Northstar Ventures (NSV) I, its first-ever early-stage fund, garnering a remarkable $140 million in capital commitments. Korea Investment Partners entered the Southeast Asia scene with a bang, announcing its inaugural $60 million Southeast Asia Fund. United States venture capital firm In-Q-Tel, Inc. (IQT) has announced the opening of a new office in Singapore.

These developments in VC fundraising underscore the evolving landscape of venture capital, reflecting a range of strategies and niches being explored by firms worldwide as they navigate the changing dynamics of the startup and investment ecosystem.

Stepping into 2024, it’s against the backdrop of remarkable resilience and adaptability that a series of transformative developments and a shifting mindset have left an indelible mark on the world of startups and venture capital. Positive signals of tailwinds are propelling startups toward profitability while refining sustainable business models with a focus on capital efficiency. Abundant VC PE dry powder has reignited dealflow, instilling hope among venture capitalists for increased investment in both emerging and established startups, poised to redefine the technology industry.

Kickstarting 2024: AI + HealthCare

In January 2024, the tech world geared up for two major events that promise to set the stage for an exciting year of technological innovations.

The first is the renowned J.P. Morgan Healthcare Conference (JPMHC), now in its 42nd year, which stands as the industry’s largest and most informative healthcare investment symposium. Held annually in San Francisco, it serves as a pivotal platform for showcasing groundbreaking healthcare technologies and trends.

In San Francisco, the JPMHC spotlighted 2023 as a robust year for mergers and acquisitions (M&A), driven by a flurry of nine M&A deals valued at over US$1 billion each that were announced towards the end of the year. The pharmaceutical giants, often referred to as Big Pharma, have been actively seeking strategic acquisitions to replenish their pipelines in response to drugs nearing patent expiration. These high-value M&A transactions primarily focused on target companies boasting late-stage assets, including marketed drugs and products with clinical proof of concept in phase 3 trials.

Meanwhile, venture capitalists (VCs) in the healthcare and life sciences sector remain well-positioned with significant capital reserves ready for deployment. Notably, new funds like Goldman Sachs’ impressive US$650 million fund, West Street Life Sciences I, have emerged with a specific focus on early- to mid-stage therapeutic companies. These companies are characterized by multi-asset portfolios and encompass tools and diagnostics firms within their investment scope, signaling a dynamic and active investment landscape within the healthcare and life sciences sectors.

The data indeed reflects a notable trend: Seed stage and modest Series A financings continue to thrive in the investment landscape. However, when it comes to larger Series A and subsequent funding rounds, a clear division persists between the ‘haves’ and the ‘have nots.’ For the fortunate few, particularly those operating in hot therapeutic areas or are armed with recent data readouts that significantly de-risk their programs, capital remains readily accessible.

A striking example of this phenomenon is demonstrated by Aiolos Bio, which secured an impressive US$250 million in a Series A round for its Phase II-ready asthma/anti-inflammatory antibody targeting the TSLP pathway—technology in-licensed from Hengrui. Aiolos Bio later astounded the market by announcing its acquisition by GSK for a staggering US$1 billion upfront, with the potential for an additional US$400 million in milestones, underscoring the value of strong data and de-risked programs.

Meanwhile, Indonesia’s leading health-tech platform, Halodoc, which offers a range of healthcare services through telemedicine, medicine delivery, lab tests, and doctor appointments via smartphones, secured a substantial $100 million in Series D funding, highlighting the continued interest in health-tech innovations.

Consumer Electronics Show (CES), originating in 1967 with 250 exhibitors and 17,500 attendees in New York City, has since evolved into a global tech extravaganza. CES not only presents the latest technological advancements but also offers a glimpse into the future of the tech world. Notably, both events share a common theme: the pervasive presence of artificial intelligence (AI). AI’s influence is palpable, whether it’s in drug development, robotics, or consumer products, reaffirming its pivotal role in shaping the future of technology.

Among the groundbreaking innovations showcased at the event, Betavolt, a startup hailing from China, introduced a truly revolutionary nuclear battery technology that promises to generate electricity continuously for an astounding 50 years without the need for recharging or maintenance.

What sets Betavolt’s creation apart is its groundbreaking integration of 63 different isotopes into a module that’s smaller than a standard coin, marking a significant leap in the field of atomic energy. This achievement challenges conventional wisdom associated with nuclear technology by achieving the remarkable feat of miniaturizing atomic energy. The battery’s compact dimensions measure just 15 x 15 x 5 millimeters, constructed from delicate layers of nuclear isotopes and diamond semiconductors. It is envisioned as a remarkable technological marvel that holds the promise of keeping electronic devices charged and fully operational for an astonishing half-century. This breakthrough ushers in a transformative era of sustainability and unprecedented longevity in the realm of portable power solutions.

ChatGPT will be shoe-horned into everything. Teamwork between Volkswagen and Cerence to harness its Chat Pro “automotive grade” artificial intelligence platform, which enables the ChatGPT integration. This expands the German marque’s existing IDA voice assistant so it can now deal with natural speech prompts for both control of the vehicle’s functionality and broader queries.

Motion Pillow revealed a self-inflating, AI-powered smart pillow designed to curb snoring. Once the system identifies snoring, the pillow gently inflates to subtly adjust the sleeper’s head position. Through the movement of 7 airbags, it dynamically adjusts the positions of the head and back, creating a comfortable breathing environment and reducing snoring. The product has been further enhanced with an increased number of airbags, the vital ring for oxygen saturation measurement, circadian rhythm lighting, and a space-saving charging system, all contributing to improved performance, usability, and adding a touch of sophistication. This side-lying posture is known to be less conducive to snoring, as it helps keep airways open. The inflation mechanism is designed to be both quiet and gradual, ensuring minimal disturbance to the sleeper.

ElliQ, the innovative care companion robot introduced by Intuition Robotics, plays a vital role in addressing the growing sense of isolation experienced by older adults in our increasingly technology-driven world. This is particularly crucial in an era when staying digitally connected is paramount due to the limitations on physical interactions. With approximately 50% of adults grappling with concerns related to social alienation and declining health, ElliQ emerges as a solution designed to bridge this gap.

ElliQ serves as an interactive tabletop health companion, thoughtfully crafted to assist older adults in maintaining their mental and social well-being. By engaging in various activities and providing companionship, ElliQ not only alleviates feelings of isolation but also encourages essential mental and social interactions. It represents a compassionate response to the challenges faced by older individuals in our technology-centric society, reaffirming the potential for technology to enhance the quality of life for all generations.

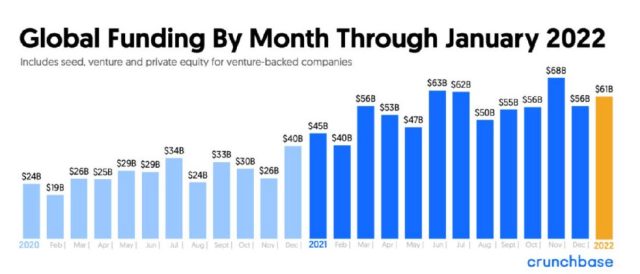

Global technology startup funding clocked in at a record $621 billion in 2021. Southeast Asia startups raised almost $25 billion marking its coming of age as an important, albeit young, tech corridor. In the first quarter of 2022, as macroeconomic and geopolitical conditions continue to evolve in a melting pot of spiralling energy costs, inflation, and interest rates coupled with a war in Europe, how will the rest of the year play out?

Data from Crunchbase seems to indicate continued strength as global startups raked in $61 billion, the 4th month above the $60 billion mark in the last 12 months. Close to $3 billion was invested globally at seed stage. Startup investors deployed another $18 billion at the early stage and just over $40 billion at the later stage and technology-growth stage. This is amidst a changing landscape where global VC funds are raising record mega funds. Andreessen Horowitz closed on a host of new funds this year, with its eighth fund at $2.5 billion, its fourth bio-related at $1.5 billion, and a third growth fund at $5 billion. Fintech specialist Ribbit Capital closed its seventh fund at just under $1.2 billion, marking its first billion-dollar fund.

While the figures for Q1 2022 Southeast Asia funding are yet to be released, funding news throughout the first three months of the year seems to suggest a good quarter for the region, especially with regard to smaller deal sizes of below $50 million.

Sequoia-backed Multiplier, a startup that enables companies to hire and pay remote workers while complying with local laws, raised $60 million at a $400 million Series B valuation with New York-based Growth Equity Tiger Global as its lead. This came barely 3 months after the company’s Series A of $13.2 million. Tiger Global, together with Cathay Innovation and Sequoia, wrote a cheque to Singapore-based AI Rudder, the leading voice artificial intelligence start-up, leading the $50 million Series B funding – less than 6 months after the company wrapped up its US$10 million Series A in November 2021. Tonik Digital Bank targeting Philippines unbanked consumers closed a $131 million round of Series B equity funding in February 2022 led by Japan’s Mizuho Bank. A VC syndicate led by Vertex and includes Prosus Ventures, AC Ventures, and East Ventures injected $30 million in Series A funding into Indonesia-based fishery and marine platform Aruna. Who would have imagined a Southeast Asia Series A round ballooning to $30 million 12 to 24 months ago!

In parallel, investors have raised concerns about the rapid pace of deals and high valuations. Having said that, it could take time for a correction to reveal itself on a market-wide scale. VC and private equity firms are sitting on immense piles of cash earmarked for startups, and competition for deals remains high. The deal-making pace of Q2 2022 will dictate the direction of venture funding for the rest of the year.

Geopolitical risk threatens to trip up venture capital’s global stride

The venture capital model is predicated upon fast growth and rapid scaling. Adding to the lingering pandemic woes is a crucible of geopolitical risk involving the world’s largest nations US, China, and Russia. For VCs, these geopolitical risks can make it more difficult to raise capital from LPs from sanctioned countries. Increased and enhanced due diligence will be necessary to avoid raising capital from sanctioned sources. Speaking to entrepreneurs in Singapore, Indonesia, and Malaysia, we observe that Southeast Asia startups have little to no dealings with Russian investors. However, some startups we spoke to have reported various delays in their supply chains, especially for parts that originate from Europe.

A Reuters report in March 2022 highlighted that global investors have pursued a re-allocation strategy into crypto and blockchain and away from real estate and bond funds, seeking exposure to a sector they believe could withstand the fallout from the Russia-Ukraine conflict. Venture capitalists invested around $4 billion in the crypto space in the last three weeks of February 2022. Bain Capital Ventures, a unit of private equity firm Bain Capital, for instance, announced in March 2022 that it is launching a $560 million fund focused exclusively on crypto-related investment.

Rising Inflation, Rising Interest Rates: A Threat To Venture Capital And Entrepreneurship?

For the first time since 2018, the Federal Reserve lifted the target for its federal funds rate by a quarter of a point, in order to battle rising inflation, thus signalling the end of a long-lasting pool of cheap capital for companies. Based on historical rate hikes globally, interest rates when they do change are expected to do so gradually. Three or four rate increases by the end of this year could add up to 1% or more to base interest rates in the US.

While higher interest rates will likely lead to a pullback in liquidity, this might have a balancing effect in that it may prevent market pricing and valuations from being driven up to unsustainable levels over the next few years.

The reduction in liquidity may also push VCs and founders to seek alternative forms of capital financing, including venture debt, which will in turn come at higher borrowing costs with venture lenders mirroring (or at least partly mirroring) any interest rate increases in the market at large.

There are two types of companies that need to be careful: companies that are “all tech and no revenue” or “all revenue and no tech”. The critical question is whether these companies are indeed solving real problems for people in a sustainable manner.

Further, such a liquidity pullback may have a disproportionate impact on later-stage technology companies that are pre-IPO (as we witnessed in Q1 2022 in the US). In this scenario, founders and investors will likely delay major liquidity events in order to prevent valuation discounts, given the recent poor performance of many newly listed technology companies.

It’s not all doom and gloom, however. Many technology companies that had a funding event in the past 12 months have likely raised more cash than needed. These companies will likely have to cut expenditures with the aim of extending their cash runways.

Companies can also raise extension rounds, offering shares at the same price as the most recent funding round. Extension rounds were common at the start of the COVID-19 pandemic as they allowed investors to double down on promising companies without having to face steep valuation uplifts amidst an uncertain trading environment.

Many companies with healthy cash flow turn to venture debt and growth debt to shore up balance sheets. A prime example in 2020 was AirBnB which turned away from equity in favour of $2 billion debt at a 10% interest rate from Silver Lake, shoring up its balance sheet despite having close to $4 billion in cash reserves already.

And not to forget that such moments can offer a silver lining for strong founders; market share can be hard to grow when times are good and competition fierce, and perhaps more easily gained during a downturn provided the company is well-financed with a strong team in place.

John Chambers, Chairman Emeritus of Cisco and founder and CEO of Palo Alto’s JC2 Ventures, shared his views that startups are nimble and flexible which works in their favour, highlighting examples of how Cisco and Amazon had trod on similar paths to becoming industry leaders.

Tight Labour Market

It is likely that the Southeast Asian tech ecosystem is entering a golden phase as the tech market continues to grow strongly over the years, speedbumps notwithstanding. Global and pan-Asian tech giants have recognised the region as a strong potential growth engine as part of their global ambitions. As these giants expand in Southeast Asia, the competition to attract and retain talent is becoming a challenge among startups and their larger counterparts. Startups are finding it tough to hire new and replacement employees and expensive to compete with their better-funded, larger, global competitors.

Speaking to regional startup founders and CFOs, we observed a few notable trends. Product, Technology, and Sales are the most challenging positions to fill. There is a growing trend of candidates who accept job offers but do not turn up for work on Day 1. Their reason: they have been offered up to 50% or even 100% more in salary to jump ship. Candidates are also asking for sky-high salaries and are attracted to “frontier” tech like crypto and Metaverse companies.

Startup CFOs tell us that they try to counter these trends with strong and regular internal communications and frequent external initiatives aimed at potential new applicants. Social media, such as LinkedIn, is a valuable tool to grow the employer brand influence of a company. A startup we surveyed is launching what it calls a “Craftsmen Program” to retain team members who have strong coding skills by providing them with visible career path progressions. Last but not least, the delayed nature of the ESOP (employee stock option plan) vesting schedule does also help with retention.

The role of debt financin

2008 (GFC), 2020 (COVID-19) and now 2022. Bumpy years where prudent leadership teams were/are eager to hold on to more cash and shore up balance sheets.

Debt financing can help companies prolong the life of expensive equity already raised. Having an extra 20% or 30% cash cushion gives leadership teams more options by extending the company’s runway, accelerating growth, and staying ahead of the competition.

As for rising interest rates, venture lenders will continue to price in risk and mirror market movements. Where bank rates edge upwards venture lenders are expected to generally mirror that movement by way of interest rate adjustments and even adjustments to warrant option coverage, all with the objective of risk-adjusted pricing. In fact, increased interest rates notwithstanding, our conversations with other regional venture debt operators point to strong deal flow in H1 2022. From Europe to India, and in Southeast Asia considering our own deal flow pipeline, indications are positive that a strong lending pace will continue into the rest of the year. However, lenders are also more cautious of who they lend to and will necessarily tighten the qualification requirements and their credit lens.