Choosing the Right Venture Lender for Your Startup

Venture debt is a financing tool that can help startups achieve business milestones while being minimally dilutive to founders and early-stage investors. It can be used to extend the runway between equity raises, thus buying time for early-stage startups to hit key benchmarks. When used thoughtfully, venture debt can act as a catalyst for accelerated growth.

Just as you would meticulously evaluate a potential business partner or new hire, conducting due diligence on your venture lender is just as essential to ensure a mutually beneficial outcome. The criteria for choosing a venture lender closely mirror those for choosing a venture equity partner – but with a few important distinctions, which arise from the differences between debt and equity financing.

In this comprehensive guide, we unveil the critical steps for performing due diligence on your venture debt lender, helping you forge a partnership that straps rockets to your growth.

Assessing Added Value

Venture debt is more than just a loan. Scrutinize the value beyond the dollars – delve into the lender’s value add – operational acumen, industry connections, and advisory capabilities. Just as a venture equity partner brings expertise and a strategic network, a venture lender should ideally be able to advise on the technicality of your financial statements – are you over-spending on marketing, or why are you budgeting large overheads for staff expansion. You would also want a venture lender to bring their network and experience to significantly amplify your growth trajectory. Engage in candid conversations about their involvement in portfolio companies and how they’ve contributed to success.

For instance, at Genesis, our portfolio companies are integral to our community. We actively champion them to a diverse array of investors, partners, and clients, both within the virtual realm and offline arenas. (#GenesisStories)

Through Thick and Thin

The road to building a successful startup will be long and filled with potholes. Whether the loan spans one or three years, mutual trust will be very important. Throughout your interactions, ask yourself, “Am I dealing with someone who understands how a start-up grows? Will they stand shoulder-to-shoulder with us through the good times and bad?”

So speak to at least three of their Founders; ask about their lender’s behaviour during the COVID pandemic or recent tech funding winter. A venture debt partner who stands by your side through adversity is a valuable ally in ensuring your startup’s resilience and growth.

Mastering Key Terms

Unlike a venture equity firm’s term sheet, the one from your venture lender might throw some unfamiliar terms your way that are worth understanding in advance:

Interest rate: This is the loan interest rate and be sure to know if it’s “fixed” or “floating”, “flat” or “annualized”. This makes a big difference in your repayments and cash flow.

Duration of loan: This is typically one to three years depending on the working capital requirement and the venture lender’s fund life. Generally, longer-term loans are attractive as they allow more time for the capital to work and generate a return.

Interest-only period: Given the cash-burn profile of startups, you can negotiate with your lender to defer paying the principal while servicing only the interest payments for an initial period of 3-6 months. In return, the lender may ask for additional upside, for example, more warrants or higher interest rates etc.

Warrants: Warrants give the lender the right to purchase equity shares at a predetermined price at a future date. This usually amounts up to 20% of the loan principal amount.

Fees: There are several fees that Founder’s should be aware of e.g. origination fee, legal fee which are typically mandatory and then there are other fees such as “Unused fees”, or “Closing fees”, that are in addition to interest payments.

Prepayment Penalties: In the happy event where your cashflow is more positive than forecasted, you may wish to pay off your debt early. Examine the penalties for early payment and there are may be creative ways to structure these penalties to mutual advantage e.g. a sliding scale expressed as a percentage of the loan as the loan period draws to a close.

Covenants: are “stress tests” that companies must meet e.g. minimum working capital, EBITDA, or revenue etc. Have a candid discussion with your lender regarding the rationale behind each covenant. Usually covenants are not meant to be putative in nature but to ensure that the startup practices financial discipline.

Due Diligence on Due Diligence

Finally, take a moment to find out how the lender conducts its own diligence. Inquire about their due diligence process, including the depth of research, the rigor of analysis, and the criteria they prioritise. A thorough, systematic approach to due diligence indicates a commitment to informed decision-making, which will serve as a strong foundation for your partnership.

Founder’s Guide to Successfully Raising Venture Debt

So you’ve caught wind of venture debt – the financing option that enables startups to secure capital while safeguarding Founder’s ownership stakes. Now, the real question is: How do you navigate the maze and successfully raise venture debt for your burgeoning business?

In this article, we will share the typical path that leads to venture debt success. Picture this as your startup’s GPS, guiding you through each pivotal step, from the first call to securing a promising term sheet.

Firstly, it is important to realise that venture lenders typically focus on startups that have revenue streams and possess equity backing. Nevertheless, it is best to initiate such discussions with venture lenders even if you are not actively fund-raising. This gives both parties the opportunity to grasp each other’s business models and find comfort working with one another.

Secondly, the process from the initial conversation to an eventual disbursement may take up to two months, depending on the depth of due diligence required and how readily you furnish the required information. A typical process looks like this:

Introductory Conversation: The first introductory call is like a first date, where both sides listen intently and get to know each other.

NDA Signing: If the initial conversation goes well, both sides will promptly sign a non-disclosure agreement (NDA) for the initial due diligence.

Initial Due Diligence: Prospective lenders will typically request key information, including:

Investor Presentation: often similar to what’s used for equity funding but with additional details on what the debt raised will be used for.

Valuation: Furnish the annual equity valuation, including history, projections, and funding details.

Historical Financials: Ideally, supply audited financial statements covering three to five years (as available).

Projected Financials: Supply a linked three-statement financial model (balance sheet, income statement, cash flow).

Customer Insights: Offer a list of major customers, past and present, indicating customer profile, concentration, and churn.

Performance Metrics: Metrics that are general and particular to your industry e.g. active user growth, monthly recurring revenue etc.

Analysis: The venture debt lender will conduct a comprehensive analysis using the provided data, typically within two weeks, resulting in a potential term sheet.

Term Sheet Presentation to your Board: Share the term sheet with your company’s board of directors, and getting their buy-in is a key step, involving them earlier in the process to prevent any unforeseen obstacles.

Negotiations: Engage in negotiations to customise the terms for a suitable structure, potentially adjusting factors such as interest rates, amortisation schedules, and timing of fund disbursement.

Final Decision: Once comparisons and negotiations are concluded, select the most fitting venture debt arrangement, which may involve equity considerations.

Thirdly, throughout this process, it is important that you have an experienced Finance manager who is conversant with building financial statements and understands what bringing debt on the company’s balance sheet means. This is because you will need to know the 4Cs:

Cost of financing: Review your cost of equity and the cost of debt by calculating the weighted average cost of capital to find the optimal mix of debt and equity.

Cap table: Understand the impact of equity and debt financing on your cap table.

Cashflow: Knowing your cashflow at present and the forecast for next 1-2 years ensures that the company is able to meet its debt obligation.

Covenants: While covenants on the terms sheets may seem restrictive at first, have a candid discussion with your lender regarding the purpose of each covenant. Ideally, the covenants should help you instill financial discipline and steer you towards sustainable profitability.

Navigating the maze of startup financing might appear intricate, yet at its heart lies a simple truth: not all financial resources are equivalent. Each startup possesses its distinct ambition, business model, and market dynamics. As a result, the blend of financing you pursue should be meticulously customised to align with your growth trajectory and overarching strategic vision. Armed with this understanding and the foundation of preliminary groundwork, you can confidently steer your startup towards a path of success.

The entrepreneurial journey is often romanticised with tales of heroic successes, but, in reality, it can be surprisingly solitary. While some successful companies have started with only two or as many as eleven co-founders, there are also numerous solo entrepreneurs who achieve remarkable accomplishments. Yet, finding a compatible co-founder can be elusive, leaving determined entrepreneurs with a crucial decision to make: go it alone or let the opportunity slip away.

As venture investors, Genesis has had the privilege of engaging founders from diverse backgrounds, building connections that stretch as far back as 2015. Throughout the years, we’ve witnessed these founders endure a rollercoaster entrepreneurial journey, braving challenges like Covid and equity winters, and, of course, embracing triumphs.

Now, we are thrilled to present our Founder’s Playbook series, a collection of curated insights and experiences gathered from these remarkable founders. This series serves as a treasure trove of wisdom, where seasoned entrepreneurs share their valuable knowledge and hard-earned lessons with the startup community.

Whether you are a budding entrepreneur navigating the early stages of your venture or an experienced founder seeking guidance in uncharted territories, our Founder’s Playbook offers a reservoir of practical tips and inspiration to fuel your own journey. Embrace the knowledge shared within and join us in fostering a community of support and growth, as we continue to shape the future of entrepreneurship together. Do get in touch with us should you be interested to share your own war stories with the founder community.

Meet Niles Toh, the solo Founder who launched FoodRazor in 2015 as a SaaS business revolutionising F&B procurement and accounting processes. His first job fresh out of university was with a B2B SaaS company in 2014, managing regional sales and business development. It didn’t take long for Niles to see the potential of B2B SaaS as a profitable business model, sparking his desire to start his own venture. His father frequently shared his experiences dealing with inefficiencies in the F&B supply chain, which sparked the idea that this was an area where he could build a solution. Efficient ordering processes for ingredients are vital for a restaurant’s success as they directly impact the quality and consistency of the dishes served. By streamlining and digitizing this process, restaurants can optimise costs and reduce waste, while ensuring a delightful dining experience for their customers. This motivated Niles to start FoodRazor to address these issues.

Niles’ Journey in his own words

Being a solo founder came with its own trials and tribulations. One of the central challenges I grappled with was the limitations in my expertise and the sheer lack of bandwidth. In hindsight, I realized the immense value and strength that a co-founder could bring to the table.Initially, I had a co-founder, who unfortunately had to leave after a year due to personal financial concerns. As we were self-funding the business at that time, we couldn’t offer the stability he needed. This valuable lesson guided my approach when starting my current venture, SuperTomato, where I have the privilege of working alongside a dedicated co-founder.

Reflecting on my journey as a solo founder, I’ve identified some key aspects I would have done differently:

Seeking a Co-Founder from the Outset:I started with a co-founder who has the technical skillset that I am lacking. When bootstrapping a company, I think it’s more important to find a co-founder with both financial resources and time to commit to the long haul. The journey often takes more time than anticipated, so having someone dedicated to the process is vital.

Building a Strong Support Network: As a solo founder, the road can be isolating, and at times, overwhelming. In retrospect, I would have actively sought out and built a robust support network of mentors, advisors, and fellow entrepreneurs to share experiences, gain insights, and stay motivated.

Expanding beyond a Domestic Market: Initially, I thought we should concentrate on Singapore and establish a strong presence here before venturing abroad. However, I have come to realise that it would have been more beneficial for us to go global right from the start and allow our paying customers to direct us toward the most promising markets for expansion. Waiting for the perfect moment to be “ready” will only hold us back.

Methodical Fundraising Process:As a founder, it’s crucial to dedicate sufficient time and effort toward identifying suitable investors. This is particularly important for new entrepreneurs who lack working experience and require more guidance. It’s essential to identify an investor who can offer valuable advice and serve as a reliable sounding board, especially during the initial stages of your entrepreneurial journey.

I wish every Founder much success in their endeavours!

In June 2021 after six years at the helm, Niles made the difficult decision to exit FoodRazor. There was a buyer ready to take over the business and he recognized that he had reached a point of burnout and no longer felt he was the right person to lead the company.

Nonetheless, his unwavering passion for solving complex problems has been reignited after a much-needed break to re-energise himself. He has since embarked on his second startup, SuperTomato.ai, a hardware-focused venture which is already profitable. This time, Niles is joined by a co-founder who is a serial entrepreneur who has started multiple successful businesses. The presence of a co-founder has made a palpable difference, providing essential support and even sparking the inception of a third startup, MonsterBuilder.ai, which emerged from SuperTomato’s requirements.

Overall, Niles would summarise his mantra as “Think Big, Start Small, Go Fast!” and the startup journey, though challenging, is fulfilling and rewarding. Follow his journey on LinkedIn.

Reporting by Nicole Lim, Investment Analyst Intern, Class of 2023.

The technology industry has been one of the most dynamic and fastest-growing sectors of the global economy in recent years. 2022 was a tale of two halves. The first half of the year (and even into Q3) continued on a positive note and benefited greatly from the COVID-induced growth on the user and innovation front. Globally, startups benefitted from the preceding year of funding strength which saw investors plough$621 billion into startups globally, including $20+ billion record funding for Southeast Asia startups.

Towards the second quarter of 2022, we surveyed our portfolio founders on the fundraising environment and business outlook. A clear majority of them were optimistic about the future, observed business growth but were already noticing the slowdown in fundraising. Amidst these uncertainties, three of our portfolio companies Deliveree, Believe, and Trusting Socialraised approximately $180 million of funding (April to June 2022).

Source: CB Insights State of Venture 2022 Report

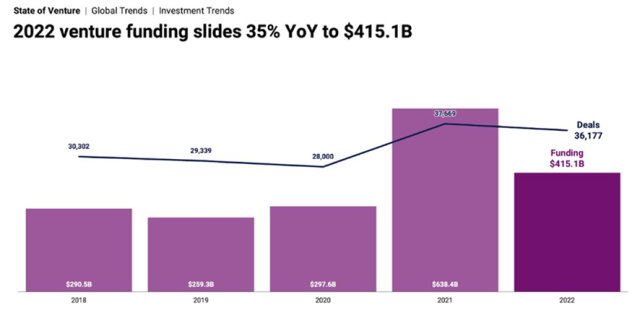

As we rolled Into the second half of 2022, and certainly more towards Q4, a new reality set in for the tech industry clouded by an array of challenges ranging from economic uncertainty, market volatility, geopolitical tensions and reverberating ripples from the pandemic. Venture investors slowed their pace of investing, due diligence took longer, valuations retreated, and we started seeing signed term sheets being delayed or even revoked. Round sizes also began shrinking and later stage startups struggled to raise growth capital while holding on to lofty valuations set during their prior fundraising rounds. Funding for tech companies globally declined to $415 billion, -35% YoY but remained healthy compared to pre-pandemic levels.

According toCartaand as a benchmark on valuation, 22% of US venture-backed companies in the US, both private and public, reduced their valuations in Q3 2022, nearly tripling year-over-year. Meanwhile, as the maxim goes, “flat is the new up” with 34% of companies witnessing a rise in their valuations — the lowest increase in five years.

While the weakening fund raising environment became more evident as the year progressed, robust fundraising in the first half of the year more than compensated for the slowdown in the second half of the year with 887 funding rounds totaling US$28.8 billion in 2022 (compared to $25.7 billion raised in 2021), according to aTechinAsia report.

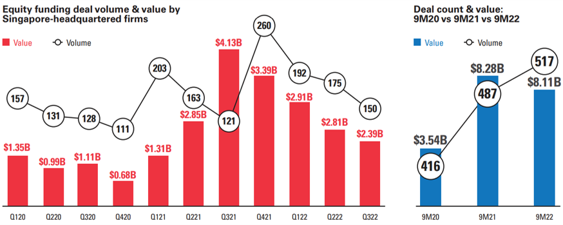

Referring to a joint DealstreetAsia and Enterprise Singapore report, Singapore-headquartered startups closed 517 deals in the first nine months of 2022 raising $8.11 billion, a little shy of the 487 deals and $8.28 billion raised in the same period of 2021, and with less dealmaking as the year prior.

VCs Prefer Early Stage, Late Stage Deals See Declining Investment Interest

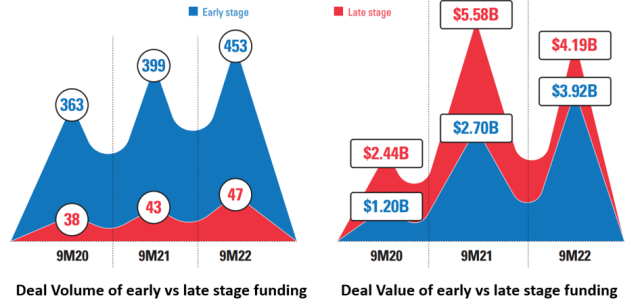

Investment statistics from the earlier report also indicate VC preference towards early stage deals, which are defined as seed through Series B rounds. Late stage are attributed to Series C and above rounds. From the graph below extracted from the DealstreetAsia and EnterpriseSG report, investors have shifted their investment dollars into a larger number of smaller, earlier venture deals. The median size of seed rounds have doubled from $1.2-1.5 million in 2021 to $2.5-3.0 million in 2022. For later stage deals, the report also highlighted a contraction of deal value for Series D and E companies by 30-50%.

In the United States, startups seeking late-stage funding are failing to attract investors as dour sentiment in the public markets and dull exit conditions make it tougher to justify higher valuations. As valuations slip to reasonable levels and startups begin to trim operating expenses to get closer to cash or EBIDTA positive levels, they may once again start to look attractive to venture and PE investors who are keen to deploy their fund capital to work.

M&As & IPOs

We observed a notable rise in private-to-private mergers and acquisitions, as publicly-listed big tech companies saw a steep decline in their share price and valuation which in turn affected the SPAC and IPO listing opportunities. Completed venture-backed acquisitions in the first three quarters of 2022 totalled $81.7 billion, according toPitchBook data, down 40.7%, from $137.8 billion in the same period the year before. No significant venture-backed tech startups went public. In total, IPO deal proceeds plummeted 94% in 2022 — from $155.8 billion to $8.6 billion — according toErnst & Young IPO report. Looking at 2023, there is an air of optimism that the IPO drought will “un-thaw” and favorable market conditions will return to allow the growing pipeline of IPO filings waiting to list – including Instacart (US), Vinfast (Vietnam), Tiktok (China), Stripe (US) and Epic Games (US).

On the M&A front,Microsoft reportedly acquired Fungible, a Santa Clara maker of data centre chips and storage device for $190m, about $134 million less than Fungible had raised in funding since its launch. Closer to home, according to a Tech in Asia report, Singapore-headquartered Amplify Health – a joint venture between AIA Group and Discovery Group – has announced its acquisition of AI-powered data analytics firm Aida Technologies. GoTo Group, the Indonesia-based tech giant, has acquired Swift Logistics Solutions for 583 billion rupiah (US$38 million).

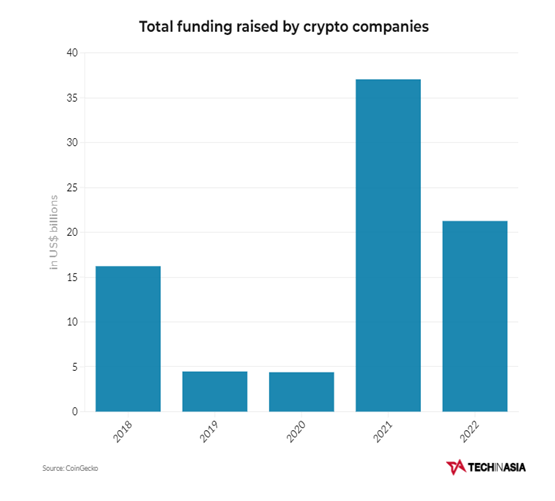

Cryptopocalypse

A year in review would be incomplete without mention of the events that took place in the crypto space which was rocked by high-profile scandals through the year. Terra Luna for example, a cryptocurrency that was launched in 2019 as a stablecoin pegged to the U.S. dollar, witnessed a crash of its Terra (LUNA) crypto token in May 2022 from $120 to $0.02, a 99.9% correction.Forbes Digital Assetestimated that nearly $60 billion was wiped out of the digital currency space.

Three Arrows Capital (3AC), a crypto hedge fund founded in Singapore and believed to be managing around $10 billion in crypto assets, incurred significant losses due to its staked Luna position. 3AC has since filed for Chapter 15 bankruptcy proceedings in the US Bankruptcy Court for the Southern District of New York to protect its US assets from creditors. And this triggered a contagion of Chapter 11 bankruptcy involving Voyager, BlockFi, Genesis Global and Celsius who had dealings with 3AC. And just before the year ended, the crypto industry experienced a Black Swan event that saw crypto exchange FTX valued at $32 billion based on its most recent funding round declared bankrupt. FTX Exchange was the world’s third largest cryptocurrency exchange specializing in derivatives and leveraged products. News around FTX’s leverage and solvency involving FTX-affiliated trading firm Alameda Research triggered a liquidity crisis when FTX’s customers demanded withdrawals worth $6 billion. FTX Token (FTT) is a utility token that provides access to the FTX trading platform’s features and services. The value of FTT fell by more than 80% within two days. The crypto industry is still reeling from a brutal 2022, having lost over US$2 trillion of its value throughout the year. Crypto companies still managed toraise a total of US$21.3 billionin funding in 2022, down 42.5% from the previous year.

Recalibration in 2023

The general consensus is that 2023 will remain challenged but withgreen shootson the horizon. Negative macro conditions are set to continue into 2023 – sustained inflation, raised interest rates, Russia v Ukraine, China-Covid slowdown etc. However, there has also been positive news flow on many of these fronts in the past weeks (e.g. inflation levelling off; China emerging quicker than expected from Covid-slowdown, China tech reawakening etc).

Taken together, and as it relates to the tech industry, it seems 2023 will provide the backdrop for a healthy recalibration period for startups globally. In Southeast Asia, for example, where most founders have not yet experienced a significant market downturn, this has been (and will continue to be) an opportunity for founders to adjust internal KPIs towards a more sustainable growth and fundraising future. Creativity loves constraint and we believe that great startups, with solid fundamentals, will emerge winners in a tight operating and funding environment.

Cash is king. VCs are encouraging their portfolio companies to conserve cash and extend their cash runway into 2024 so as to be able to operate through some of these macro headwinds. To that end, it’s worth noting that the companies in Genesis Fund I Portfolio have a weighted average cash runway of approximately 17 months this quarter (up from 13.5 months in Q3 2022).

Profit before growth. Founders are expected to be more disciplined around spending and investors are edging these startups to turn “profitable”, the definition of which is wide, but in these times has come to prioritise a meaningful and sustainable business model.

Talent stocking. Hiring exceptional talent used to come at a premium but with many startups downsizing, startup founders can now hire more prudently with less pressure on the P&L. In Southeast Asia, it’s been reported that retrenched executives from tech companies (and new job seekers) are actively in the market looking for opportunities but with more modest salary expectations.

Dry powder. Venture firms have continued to raise record capital, even as startups received far less money than they did in 2022. Dry powder was estimated to be as high as $1.3 trillion globally for private equity and $580 billion globally for VC. While we do not expect VCs to invest at a pace comparable to 2021, there is pressure stemming from fund size, duration to deploy and the need to put capital to use. As previous downturns have clearly shown, investors with dry powder will find it a rewarding time to deploy capital, amidst more reasonable valuations and the ability to set better deal terms.

2023 Hot VC Target Sectors

January is a hotbed for new tech innovation unveiled to consumers through the annual Consumer Electronics Show held in Las Vegas USA. The 2023 show is focused on a number of areas, including the metaverse and Web3, digital health, sustainability, automotive and mobility, and human security for all. There was strong participation from Asia which include those from South Korea, which number more than 500 and include the likes of Samsung, SK, Hyundai Motor and LG, while just under 150 exhibitors hail from Taiwan. We highlight some interesting technology showcased at CES:

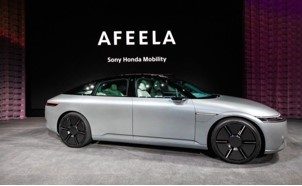

Sony teamed up with Honda to exhibit a new brand of electric vehicle called the Afeela. The Afeela logo appears on a narrow screen, or “media bar,” on the vehicle’s front bumper. This can also interact with people outside the vehicle and share information such as the weather or the car’s state of charge. Unlike the car Sony showed off at CES 2020, this car is expected to hit the North American roads in 2026. Japan and Europe will follow.

The battery-operated WasteShark by the Dutch firm RanMarine Technology is an autonomous surface vessel designed to remove algae, biomass, and floating pollution such as plastics from lakes, ponds, and other coastal waterways. At least 14 million tons of plastic end up in the ocean every year, and plastic makes up 80% of all marine debris found from surface waters to deep-sea sediments. Marine species ingest or are entangled by plastic debris, which causes severe injuries and death.

Canadian-based eSight Eyewear plans to display a headset designed to help people with visual impairments such as age-related macular degeneration (AMD). AMD is an eye disease that can blur your central vision. It happens when aging causes damage to the macula — the part of the eye that controls sharp, straight-ahead vision. The macula is part of the retina (the light-sensitive tissue at the back of the eye). AMD happens very slowly in some people and faster in others. If you have early AMD, you may not notice vision loss for a long time; hence the importance of regular eye exams. Once the user puts on the device, they will be able to see distinct features such eyebrows, mouth and eyes.

Singapore-based Igloo Company will show off its second generation of smart padlocks at CES, including a slimmed-down fingerprint-based model and another featuring enterprise-grade security. The latest smart padlocks will ship in the spring. The keypad-based Padlock 2 builds on the company’s original Bluetooth-enabled smart lock by manufacturing it to military standards, including a hardened steel case. The Padlock 2 gets eight months out of a single charge of its lithium battery (the original relied on disposable batteries), and its shackle can withstand up to 15kN of cutting force, 5kN of pulling force, and 100Nm twisting force.

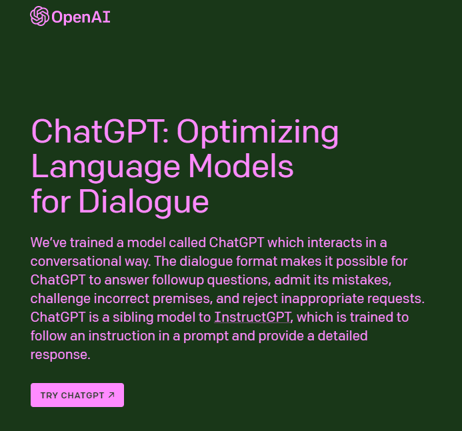

And last but not least, there has been immense interest in generative AI since ChatGPT came online and mesmerised consumers with its ability to provide real-time chat responses (see below). In 2019, Microsoft invested $1 billion in OpenAI, the tiny San Francisco company that designed ChatGPT. Microsoft is now poised to challenge Big Tech competitors like Google, Amazon and Apple with a technological advantage as it is rumoured to be in talks to invest another $10 billion in OpenAI. See the picture below (right column) where we tested Open AI’s ability to write a short paragraph on electric vehicles. Try it athttps://chat.openai.com/chat