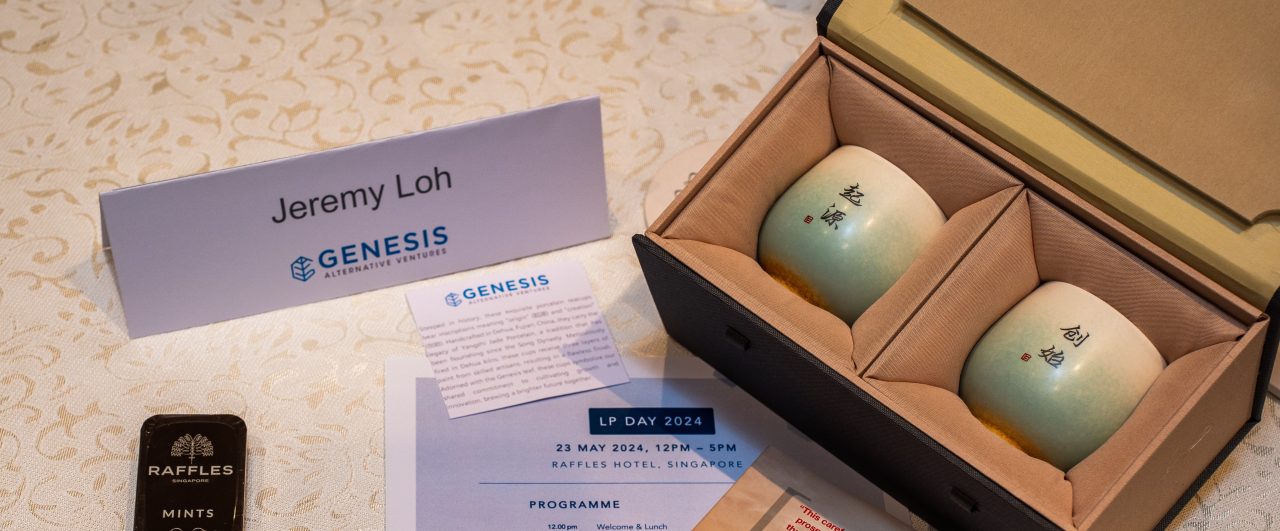

We were delighted to host our investors, partners, portfolio companies, and special guests for our annual Genesis LP Day at the iconic Raffles Hotel on 23 May 2024.

It was a fantastic gathering, filled with insightful discussions and a wonderful sense of community and we are grateful to overseas guests who travelled from Hong Kong, Indonesia, Korea, Japan, Malaysia, Thailand, and USA to join us

In addition to sharing about the performance of our Funds, our guests were treated to an insightful line-up of speakers:

Chin Hwee TAN (Energy Market Authority (EMA) Authority) explores the new multi-polar world in his latest book, “Economic Success: Fate or Destiny?” to the upcoming generation with the tools to understand and navigate this evolving landscape.

Ian Potter (Foundational Capital) on energy trends: “We’re adept at finding new ways to use energy, but less adept at finding new ways to produce it.” A thought-provoking perspective on the energy market’s future.

Bruno ROCHE (New Mutualism – The Economics of Mutuality) on responsible capitalism: Bruno offered valuable insights on the future of capitalism, emphasizing responsible business, sustainability, ESG, and mutual value creation. (Read his highly-recommended his book online for free here.)

The day continued with a Portfolio Showcase featuring six of our visionary founders who shared their aspirations and plans:

As a special thank you, we presented everyone with a unique gift: a pair of handcrafted porcelain teacups inscribed with 起源 (qǐyuán, meaning “origin”) and 创始 (chuàngshǐ, meaning “creation”). Each cup also features the Genesis leaf symbol, representing our shared commitment to cultivating growth and innovation, and ultimately, brewing a better future together.

Relive the afternoon’s highlights with our Recap Reel:

The success of any startup is inherently tied to the effectiveness of its financial management, making the role of the Chief Financial Officer (CFO) a cornerstone of the company’s growth trajectory. However, the decision to hire a CFO must be well-timed, taking into account the specific needs and stage of the startup. In this article, we have outlined the critical factors about when, what, and how to select a CFO for your startup.

When to Bring Onboard a CFO

Founders often opt to manage the finance function themselves or work with an accountant until they reach Series C or even later stages. This approach can be acceptable, particularly if the founder has a finance or banking background (although it can be a significant distraction for them!). Alternatively, it might work if their investors are actively involved in daily operations. However, linking the decision to hire a CFO solely to the funding stage, rather than considering the internal business needs, can be detrimental to the startup. It not only distracts the founder but also deprives them of a valuable, independent perspective during the crucial early scaling phase of their business.

“Once a startup has achieved product-market fit, and can afford an experienced CFO, it should start looking to fill that role … [to] help the CEO in fine-tuning pricing, tracking unit economics, evaluating alternative business strategies through a financial lens, and figuring out the funding roadmap”

Jaideep Lakshminarayanan, CFO of the AI fintech Trusting Social, recommends that once a startup has achieved product-market fit, and can afford an experienced CFO, it should start looking to fill that role. That person would help the CEO in fine-tuning pricing, tracking unit economics, evaluating alternative business strategies through a financial lens, and figuring out the funding roadmap. Having the CFO be a strategy partner at the C-suite is impactful, since many founding teams are from tech or product backgrounds.

Similarly, Kelvin Li, CFO of the market research and data analytics startup, Milieu Insight, emphasizes two primary considerations for determining the right time to bring in a CFO, primarily concerning fundraising and scaling. During institutional funding rounds, having a CFO onboard becomes vital, as fundraising can be time-consuming. A skilled CFO can streamline the process, allowing the leadership team to focus on other business aspects. Additionally, a CFO’s guidance on deal structure ensures fair terms and maximizes value for existing shareholders. With growing scale, setting up entities in multiple markets requires substantial attention and time, necessitating a CFO’s focus on these intricate operational and regulatory aspects, enabling successful market expansion.

What to Look for in a Startup CFO

The responsibilities of a startup CFO transcend traditional financial stewardship. Their role demands a specific skill set tailored to the complexities of a dynamic startup environment. This includes proficiency in financial planning, financial modelling, fundraising, treasury management, strategic thinking, tax planning, and ensuring compliance with a range of financial, tax, and employment laws.

“A startup is expected to take some time to achieve cashflow breakeven, so having a thorough understanding of the revenue and cost levers enables the company to manage its cash flow effectively before it achieves profitability,” says Kelvin from Milieu Insight.

“A startup is expected to take some time to achieve cashflow breakeven, so having a thorough understanding of the revenue and cost levers enables the company to manage its cash flow effectively before it achieves profitability”

Furthermore, there are many unknown risks that a startup has a deal with. Therefore a startup CFO must possess forward-thinking abilities, capable of envisioning the broader landscape, preempting potential hurdles, and identifying opportunities – while articulating this clearly to financial and non-financial stakeholders, both internally and externally.

“The startup environment is super fast-paced and a CFO should be adaptable to change and capable of making quick and informed decisions – often without complete financial information,” says Dominic Ong, CFO of digital wealth platform, Endowus.

“The startup environment is super fast-paced and a CFO should be adaptable to change and capable of making quick and informed decisions – often without complete financial information.”

Relationship-building and risk-mitigation skills are just as important. Jaideep adds that, “a startup CFO serves as the primary point of contact for the company with investors and strategic partners, utilizing external market insights, and identifying potential acquisition prospects. Additionally, the CFO can play a defensive role by pinpointing various risks within the business, such as customer concentration, currency exposure, and contractual vulnerabilities, and taking proactive measures to mitigate these risks.

How to Choose the Right CFO for Your Startup

Hiring the right CFO for your startup is a critical decision. Here are some strategies for finding and selecting the ideal candidate:

Figure out a Hiring Model

Startup Founders often face the challenge of juggling multiple responsibilities, making the task of financial management particularly demanding. Nevertheless, the availability of accurate, real-time financial data and strategic insights remains crucial for making informed decisions that can significantly impact the company’s trajectory.

When considering hiring a CFO, startups can choose from different models, including full-time/in-house, interim, or fractional, depending on their stage, business complexity, and budget constraints. Opting for a fractional CFO can provide the necessary level of expertise within a limited budget.

Unlike consultants who simply recommend a strategy, fractional leaders have full ownership of the role and function within the organization, and are working towards KPIs and outcomes. They engage in strategic planning, execute initiatives, measure progress, and adapt strategies as needed.

According to Elena Chow, Founder of ConnectOne, a talent solutions firm focused on startups, “Engaging a fractional CFO is a practical option for early-stage startups, providing the necessary expertise and resources to streamline financial operations without the need for a full-time team or a significant financial commitment. Such an arrangement can work well if it is structured with very specific outcomes and deliverables.”

“Engaging a fractional CFO is a practical option for early-stage startups, providing the necessary expertise and resources to streamline financial operations without the need for a full-time team or a significant financial commitment. Such an arrangement can work well if it is structured with very specific outcomes and deliverables.”

Consult your lead VC or Advisory Board member with deep industry experience to help assess your startup’s needs and identify suitable CFO candidates. Your VC has worked with many CFOs and their experience can be invaluable in recommending a candidate with a proven track record and culture-fit. Your VC or Board member can also partner you in the interview process and act as a sounding board.

Technical Qualifications

An effective startup CFO offers deep strategic financial expertise that complements the technical skills of the C-suite and aligns with the company’s core business objectives. They must have the capability to identify essential metrics for effective business management and enforce a structured approach to tracking and reporting these metrics. This ensures that the decision-making process within the C-suite is both well-informed and timely.

Key prerequisites for a competent startup CFO include:

A minimum of 10 years of industry experience, preferably in Corporate Finance.

Background experience from “Big 4” accounting firms, along with CPA or MBA certifications.

Previous involvement in fundraising, mergers and acquisitions (M&A), and initial public offerings (IPOs).

Proven experience in leading startups through successive scale-ups.

A history of serving as a reliable sounding board for the CEO, particularly highly stressful situations

Some operational experience in identifying inefficiencies and bottlenecks and devising actional plans to address them.

Essential Soft Skills

According to Dominic, a startup CFO needs to be a forward-thinker, capable of seeing the big picture, and anticipating potential challenges and opportunities – while articulating this clearly to financial and non-financial stakeholders both internally and externally. While there is no “one-size-fits-all”, there are certain attributes that are critical for startup CFOs, which include:

Conflict Management: As the role of finance is to provide checks and balances, the CFO’s ability to disagree and forge a compromise is an essential skill.

Change management: A top startup CFO must be comfortable with change and ambiguity, adapting quickly to dynamically evolving circumstances.

Relationship Building: Beyond being a “cost gatekeeper”, a CFO capable of fostering strong relationships both internally and externally can help channel collective resources and efforts toward accomplishing the company’s mission.:

Emotional Self-Mastery: Because startups will go through business pivots and funding crises, an essential trait that a CFO should have is keeping a cool head as you work through the challenges together.

Creative Problem-solving: A startup’s growth journey is often non-linear, so a CFO must be able to devise customised solutions for dynamic situations must be able to juggle and prioritize multiple workstreams

Gather Feedback

All the CFOs in this article agree that honesty and integrity are non-negotiables, therefore carrying out due diligence on the candidate is paramount. Conducting comprehensive background checks, including thorough network assessments with the candidate’s former colleagues, business partners, and clients, is crucial to verifying their professional history and character. Your VC, trusted advisor, or Board Member can assist with a confidential check regarding their ethical standards, work ethic, and overall performance. This process not only safeguards your company from potential risks but also allows you to make an informed decision that aligns with your organization’s values and long-term objectives.

The ultimate goal is for the CFO to become a strategic partner, contributing to long-term planning and decision-making, including pricing, expansion, acquisitions, and more. It is multi-faceted and evolves as the company grows. Timing the hire correctly, understanding the specific skills and qualifications required, and adopting the right hiring model are crucial for ensuring your startup’s financial health and long-term success. A skilled CFO can help guide your startup through the challenges of scaling while contributing significantly to bringing your dream to life.

Choosing the Right Venture Lender for Your Startup

Venture debt is a financing tool that can help startups achieve business milestones while being minimally dilutive to founders and early-stage investors. It can be used to extend the runway between equity raises, thus buying time for early-stage startups to hit key benchmarks. When used thoughtfully, venture debt can act as a catalyst for accelerated growth.

Just as you would meticulously evaluate a potential business partner or new hire, conducting due diligence on your venture lender is just as essential to ensure a mutually beneficial outcome. The criteria for choosing a venture lender closely mirror those for choosing a venture equity partner – but with a few important distinctions, which arise from the differences between debt and equity financing.

In this comprehensive guide, we unveil the critical steps for performing due diligence on your venture debt lender, helping you forge a partnership that straps rockets to your growth.

Assessing Added Value

Venture debt is more than just a loan. Scrutinize the value beyond the dollars – delve into the lender’s value add – operational acumen, industry connections, and advisory capabilities. Just as a venture equity partner brings expertise and a strategic network, a venture lender should ideally be able to advise on the technicality of your financial statements – are you over-spending on marketing, or why are you budgeting large overheads for staff expansion. You would also want a venture lender to bring their network and experience to significantly amplify your growth trajectory. Engage in candid conversations about their involvement in portfolio companies and how they’ve contributed to success.

For instance, at Genesis, our portfolio companies are integral to our community. We actively champion them to a diverse array of investors, partners, and clients, both within the virtual realm and offline arenas. (#GenesisStories)

Through Thick and Thin

The road to building a successful startup will be long and filled with potholes. Whether the loan spans one or three years, mutual trust will be very important. Throughout your interactions, ask yourself, “Am I dealing with someone who understands how a start-up grows? Will they stand shoulder-to-shoulder with us through the good times and bad?”

So speak to at least three of their Founders; ask about their lender’s behaviour during the COVID pandemic or recent tech funding winter. A venture debt partner who stands by your side through adversity is a valuable ally in ensuring your startup’s resilience and growth.

Mastering Key Terms

Unlike a venture equity firm’s term sheet, the one from your venture lender might throw some unfamiliar terms your way that are worth understanding in advance:

Interest rate: This is the loan interest rate and be sure to know if it’s “fixed” or “floating”, “flat” or “annualized”. This makes a big difference in your repayments and cash flow.

Duration of loan: This is typically one to three years depending on the working capital requirement and the venture lender’s fund life. Generally, longer-term loans are attractive as they allow more time for the capital to work and generate a return.

Interest-only period: Given the cash-burn profile of startups, you can negotiate with your lender to defer paying the principal while servicing only the interest payments for an initial period of 3-6 months. In return, the lender may ask for additional upside, for example, more warrants or higher interest rates etc.

Warrants: Warrants give the lender the right to purchase equity shares at a predetermined price at a future date. This usually amounts up to 20% of the loan principal amount.

Fees: There are several fees that Founder’s should be aware of e.g. origination fee, legal fee which are typically mandatory and then there are other fees such as “Unused fees”, or “Closing fees”, that are in addition to interest payments.

Prepayment Penalties: In the happy event where your cashflow is more positive than forecasted, you may wish to pay off your debt early. Examine the penalties for early payment and there are may be creative ways to structure these penalties to mutual advantage e.g. a sliding scale expressed as a percentage of the loan as the loan period draws to a close.

Covenants: are “stress tests” that companies must meet e.g. minimum working capital, EBITDA, or revenue etc. Have a candid discussion with your lender regarding the rationale behind each covenant. Usually covenants are not meant to be putative in nature but to ensure that the startup practices financial discipline.

Due Diligence on Due Diligence

Finally, take a moment to find out how the lender conducts its own diligence. Inquire about their due diligence process, including the depth of research, the rigor of analysis, and the criteria they prioritise. A thorough, systematic approach to due diligence indicates a commitment to informed decision-making, which will serve as a strong foundation for your partnership.

Superbank and Genesis Alternative Ventures Launch IDR 600 Billion Financing Solution for Innovative Indonesian Startups

The collaboration marks a significant milestone as Superbank expands support to local entrepreneurs and MSMEs

Targeting VC-backed, high-growth technology startups in Indonesia

Jakarta, 31 August 2023 – PT Super Bank Indonesia (Superbank) and Genesis Alternative Ventures (Genesis), Southeast Asia’s prominent venture lender, have launched a financing solution, with both entities committing up to IDR 600 billion to back innovative Indonesian startups.

The financing solution combines the principles of conventional bank credit and venture capital investing to target Indonesian technology startups while extending working capital to technology startups with minimum dilution of shareholder equity.

This collaboration between Superbank and Genesis underscores the determination of both entities to empower startups in Indonesia, particularly those at the Series B or C stage, to realize their full potential.

Tigor M. Siahaan, President Director of Superbank, said, “As the largest digital economy in Southeast Asia, which is expected to grow eight times from IDR 632 trillion in 2020 to IDR 4,531 trillion in 2030, Indonesia has the potential and opportunity to further develop local startups and their ecosystem¹. We are thrilled to partner with Genesis to provide a powerful financing avenue for innovative Indonesian startups. In today’s dynamic business environment, access to funding is crucial for these innovative ventures to thrive. This partnership exemplifies Superbank’s unwavering commitment to supporting local entrepreneurs and MSMEs and driving sustainable growth.”

Jeremy Loh, Co-founder & Managing Partner Genesis Alternative Ventures, said, “Indonesia is brimming with opportunities in terms of local startups and tech talents. Genesis and Superbank share the same commitment in tapping the huge potential of this sector and supporting more startups in Indonesia given the notable 60% year-on-year² decline in venture capital funding for startups the Asian region has witnessed.”

This collaboration marks a significant milestone in Superbank’s transformation into a digitally-focused bank that just started 6 months ago.

For further information, please contact:

Andre Sebastian Public Relations Lead Superbank public.relations@superbank.id

Keshie Hernitaningtyas Brightminds for Superbank superbank@brightminds.co.id

About Superbank PT Super Bank Indonesia (Superbank) is a bank that’s currently transforming into a digital-based services bank. Superbank is the new brand that replaces PT Bank Fama International, a commercial bank that was founded in Bandung, 1993 which was taken over by the EMTEK Group, Grab and Singtel in 2021. Superbank has received various awards, such as “The Most Efficient Bank in the Group of Banks Based on Core Capital (KBMI) 1 Category” from Bisnis Indonesia Financial Award (BIFA) 2022. As a newcomer in the Indonesian digital banking sphere, Superbank has a mission to expand access to credit for MSME customers in managing their businesses, provide innovative solutions for retail customers, and foster collaboration through one of the industry’s most extensive ecosystems.

For further information on Superbank, please visit www.superbank.id.

About Genesis Alternative Ventures Genesis Alternative Ventures is Southeast Asia’s leading private lender to venture and growth stage companies funded by tier-one VCs. Genesis is founded by a team of venture lending pioneers who have backed some of Southeast Asia’s best loved companies. Armed with a strong reputation among entrepreneurs and investors, Genesis is a trusted partner in empowering corporate growth while minimising shareholders’ equity dilution. Genesis was founded by Ben J Benjamin, Dr Jeremy Loh and Martin Tang in 2019.

For further information on Genesis Alternative Ventures, please visit www.genesisventures.co.

Founder’s Guide to Successfully Raising Venture Debt

So you’ve caught wind of venture debt – the financing option that enables startups to secure capital while safeguarding Founder’s ownership stakes. Now, the real question is: How do you navigate the maze and successfully raise venture debt for your burgeoning business?

In this article, we will share the typical path that leads to venture debt success. Picture this as your startup’s GPS, guiding you through each pivotal step, from the first call to securing a promising term sheet.

Firstly, it is important to realise that venture lenders typically focus on startups that have revenue streams and possess equity backing. Nevertheless, it is best to initiate such discussions with venture lenders even if you are not actively fund-raising. This gives both parties the opportunity to grasp each other’s business models and find comfort working with one another.

Secondly, the process from the initial conversation to an eventual disbursement may take up to two months, depending on the depth of due diligence required and how readily you furnish the required information. A typical process looks like this:

Introductory Conversation: The first introductory call is like a first date, where both sides listen intently and get to know each other.

NDA Signing: If the initial conversation goes well, both sides will promptly sign a non-disclosure agreement (NDA) for the initial due diligence.

Initial Due Diligence: Prospective lenders will typically request key information, including:

Investor Presentation: often similar to what’s used for equity funding but with additional details on what the debt raised will be used for.

Valuation: Furnish the annual equity valuation, including history, projections, and funding details.

Historical Financials: Ideally, supply audited financial statements covering three to five years (as available).

Projected Financials: Supply a linked three-statement financial model (balance sheet, income statement, cash flow).

Customer Insights: Offer a list of major customers, past and present, indicating customer profile, concentration, and churn.

Performance Metrics: Metrics that are general and particular to your industry e.g. active user growth, monthly recurring revenue etc.

Analysis: The venture debt lender will conduct a comprehensive analysis using the provided data, typically within two weeks, resulting in a potential term sheet.

Term Sheet Presentation to your Board: Share the term sheet with your company’s board of directors, and getting their buy-in is a key step, involving them earlier in the process to prevent any unforeseen obstacles.

Negotiations: Engage in negotiations to customise the terms for a suitable structure, potentially adjusting factors such as interest rates, amortisation schedules, and timing of fund disbursement.

Final Decision: Once comparisons and negotiations are concluded, select the most fitting venture debt arrangement, which may involve equity considerations.

Thirdly, throughout this process, it is important that you have an experienced Finance manager who is conversant with building financial statements and understands what bringing debt on the company’s balance sheet means. This is because you will need to know the 4Cs:

Cost of financing: Review your cost of equity and the cost of debt by calculating the weighted average cost of capital to find the optimal mix of debt and equity.

Cap table: Understand the impact of equity and debt financing on your cap table.

Cashflow: Knowing your cashflow at present and the forecast for next 1-2 years ensures that the company is able to meet its debt obligation.

Covenants: While covenants on the terms sheets may seem restrictive at first, have a candid discussion with your lender regarding the purpose of each covenant. Ideally, the covenants should help you instill financial discipline and steer you towards sustainable profitability.

Navigating the maze of startup financing might appear intricate, yet at its heart lies a simple truth: not all financial resources are equivalent. Each startup possesses its distinct ambition, business model, and market dynamics. As a result, the blend of financing you pursue should be meticulously customised to align with your growth trajectory and overarching strategic vision. Armed with this understanding and the foundation of preliminary groundwork, you can confidently steer your startup towards a path of success.

In this issue of our House View, we shine the spotlight on an extremely talented individual within the Genesis ecosystem, Tom Kim, founder and CEO of Deliveree.

Deliveree was established in 2015 with a core focus on the efficient transportation of commercial goods and large items across Indonesia, the Philippines, and Thailand. The company set out to address the challenges associated with transportation inefficiencies and the high cost of logistics. The company is projected to exceed $100 million in GTV this year. Deliveree has a team of 550 dedicated employees and a robust network of 100,000 drivers operating on its platform. Deliveree has successfully raised $109 million in capital to date.

The problem Deliveree is solving is the prevalence of one-way deliveries leading to empty return trips. In short, Deliveree devised a dynamic marketplace that connects independent drivers and trucking companies on the supply side, with tens of thousands of customers driving the demand. Matching supply to demand in this manner is no easy task, yet Deliveree managed to overcome this challenge and achieve a utilisation rate of nearly 70%, which surpasses the industry average that sits at under 50%. This accomplishment has direct positive effects on both the environment and productivity, as fuel and time are optimized. Moreover, it benefits independent truckers who rely on commission-based earnings, thereby allowing them to earn more. Notably, customers such as UPS, DHL, Philip Morris, Suntory, and Lotus’s (formerly Tesco) can now leverage an asset-light approach, booking trucks as and when necessary, which helps streamline their balance sheets.

The Genesis team first engaged with Deliveree in 2016 for discussions around debt financing and then again in April 2020. Deliveree stood out to Genesis for several reasons, including healthy, mid-teen gross margins, a dedicated and experienced management team, with a strong commitment to resolving logistical challenges. Genesis and Deliveree shook hands on a first debt facility soon after and Genesis subsequently participated in an additional round that saw Deliveree complete a massive $70 million Series C funding in June 2022.

Genesis’ investment philosophy includes a dedication to supporting startups with meaningful impact objectives. We work closely with our portfolio companies, assisting them in identifying and implementing essential impact and environmental, social, and governance (ESG) concepts throughout Southeast Asia. Deliveree is amongst the first of our portfolio companies to demonstrate a bold commitment to these principles. In May 2023, Deliveree published its inaugural report detailing its ESG and impact achievements. We are proud to have played a small part in Deliveree’s journey in this regard.

Please enjoy this Q&A with Tom.

Tell us more about your declaration of war against empty trucks and how far has Deliveree’s technology and marketplace come?

Tom Kim [TK]: Deliveree connects thousands of truck drivers and cargo shippers through its dynamic marketplace where they can find and fulfil orders every day. We are constantly upgrading our tech stack which is now third generation and going onto its fourth evolution. These improvements are based on the feedback of our loyal business customers.

Our drivers use our proprietary mobile app that shows them the live bid price and lets them accept delivery orders on the go, even while they are on a specific route. The app also helps Deliveree to track the trucks’ location and offer a hyper-local view of truck capacity for route planning.

Using our Big Data and predictive analytics, we “smart assign” bookings to drivers, which enables them to create optimised routes and schedules. On average, our drivers achieve utilisation rates ranging from 60% to 80%, with an average of 70%, as they criss-cross the map every day picking up and dropping off loads for a diverse range of customers.

In turn, this allows customers of all sizes to access affordable, flexible, and scalable trucking and cargo shipping solutions in a way that significantly increases efficiency and reduces cost. We can achieve these utilisation rates within metropolitan areas and even across larger areas such as Java Island in Indonesia, Luzon Island in the Philippines, and the Bangkok Metropolitan Area in Thailand.

Please elaborate on Deliveree’s “smart assignments” technology and how that sets you apart from traditional logistics providers?

TK: Deliveree’s “smart assignments” technology sets it apart from traditional logistics providers. This technology, driven by intelligent algorithms applying massive historical data sets, assigns trucks to bookings in the most optimal locations and times. This maximises truck utilisation and minimises empty driving distances, resulting in higher efficiency.

We believe that Big Data is the key to logistics evolution in Southeast Asia. Our success hinges on the ability to gather, combine, and effectively use data sets to tackle the region’s logistics efficiency challenges. In contrast, many competitors are still in the early stages of their first or second-generation tech, lagging behind Deliveree in user experience, features, integration capabilities, toolsets, and most importantly, Big Data and predictive analytics.

A key feature of smart assignments is the ability to estimate the duration of each booking based on massive historical data sets from seven years of operations. This allows the algorithm to help drivers build booking schedules with routes and timing that fit and flow together from one booking to the next, further streamlining logistics operations. By leveraging the power of Big Data, Deliveree aims to precisely predict booking durations, resulting in fully optimised truck schedules. This innovative approach not only solves the problem of empty trucks on the road but also addresses the elusive issue of empty backhauls (the holy grail of logistics). Moreover, it helps to reduce traffic congestion, minimise environmental emissions, increase driver earnings, and lower customer shipping costs. While it may seem too good to be true, Deliveree is working towards this future every day through significant investments in Big Data sets.

What was your motivation for setting up a formal ESG reporting process?

TK: Deliveree’s solution benefits various stakeholders, including truck drivers, businesses with goods to deliver, and even the environment. Our latest ESG report is available here.

We address the challenges faced by independent owner-operator drivers and small family trucking companies with unstable income and limited job opportunities. Through onboarding and continuous training, drivers qualify for jobs with larger enterprises that have strict requirements, such as certifications for occupational health and safety (OSHA) to enter warehouses and logistics facilities. Additional certifications, like defensive driving for energy clients and perishable goods handling for FMCG clients, are also provided.

Our comprehensive training and certification program prepares drivers for the new gig economy. Together with our mobile app, they secure delivery jobs that significantly boost their earnings, often up to 2.3 times more. This empowers businesses to connect with reliable and qualified drivers for their transportation needs while contributing to better route optimisation and environmental sustainability.

In our ESG sustainability report, you will see how our smart algorithms optimise delivery routes, providing bookings to trucks in the right place at the right time.

This increases their utilisation and decreases the distances those trucks drive while empty. Additionally, businesses can leverage Deliveree’s partial loading services, enabling them to send goods, cargo, and packages without needing to rent a full vehicle. Our algorithm calculates the most optimal and efficient route by combining cargo from multiple businesses, ensuring efficient deliveries.

Who helped you with the process and the thinking behind your ESG initiative?

TK: As part of Genesis’ venture debt to Deliveree back in January 2021, we made a commitment to Genesis Impact and E&S framework where we will start to develop a basic idea around impact development goals and objectives. However, at that time we were focusing on growth and not ready to devote resources to a deep dive to evaluate our potential ESG impact.

This changed in 2023 when our database and data science resources became substantially more sophisticated. Deliveree’s servers process vast amounts of data related to our millions of transactions and core operational functions. So the data was already there, but the hard part was building the right queries to extract, clean, and draw conclusions from the data to tell the ESG story along the main themes we outlined.

With guidance and support from Genesis who made introductions to experts and consultants in this field, we identified four key ESG impact themes that align with UN Sustainability Development Goals. Then we pursued the data extraction and analysis to validate our achievements along these themes.

We started by delving into the essence of Deliveree’s core business. While the impact was already evident, the challenge was quantifying and measuring this impact in a tangible manner. Genesis and Deliveree held several discussions, engaging in informative and collaborative discussions on quantifying impact using our existing data.

By documenting our ESG and impact achievements, we aim to strengthen our credibility in the eyes of investors, partners, clients, and vendors. This commitment to ESG impact reflects Deliveree’s dedication to sustainability and responsible business practices.

What are some key highlights of Deliveree’s ESG sustainability report for 2022/2023?

TK: At a high level, I am very proud to share the following achievements:

Emissions Reduction: Deliveree’s “smart assignments” has reduced CO2 emissions by over 3 million kilograms, equivalent to planting 143,000 trees (UNSDG: Climate Action).

Road Traffic Reduction: Through efficient truck assignments, Deliveree has decreased truck road usage by 5.3 million kilometres, equivalent to 7 return trips between Earth and the Moon. (UNSDG: Infrastructure and Sustainable Cities).

Income Acceleration: Independent drivers and small trucking businesses on Deliveree’s platform experienced significant earnings growth, with average hourly earnings increasing by 2.8 times for 73% of vendors and total earnings increasing by 2.3 times for 82% of vendors. (UNSDG: No Poverty and Decent Work).

New Economy Education: We provided extensive education to drivers, offering an average of 44 instructional hours per vendor, enabling them to thrive in the mobile app and gig economy. (UNSDG: Decent Work and Reduced Inequalities).

We have gained a strong reputation for our customer-oriented services. However, we also want to recognise the unsung heroes behind our success: the countless truck drivers who own and operate their own vehicles, as well as the small family businesses that own and manage their own fleets. Our platform empowers them to control their financial futures, leading to a positive impact on their respective communities.

What was the response to your report?

TK: Unfortunately, the response from the media and investment community was not as warm as we had hoped. From this, we realised that ESG and impact investing are still relatively young fields, and there is a limited track record of long-term performance data. In this respect, I am proud that Deliveree is ahead of the pack when it comes to monitoring our ESG and impact.

What are your business plans for the next few years?

TK: We are commencing our last private fundraising in the second half of 2023 with plans to IPO in Indonesia in late 2025/early 2026. To coincide with these capital markets plans, our consolidated group will reach EPS break-even by 4Q 2025.

The entrepreneurial journey is often romanticised with tales of heroic successes, but, in reality, it can be surprisingly solitary. While some successful companies have started with only two or as many as eleven co-founders, there are also numerous solo entrepreneurs who achieve remarkable accomplishments. Yet, finding a compatible co-founder can be elusive, leaving determined entrepreneurs with a crucial decision to make: go it alone or let the opportunity slip away.

As venture investors, Genesis has had the privilege of engaging founders from diverse backgrounds, building connections that stretch as far back as 2015. Throughout the years, we’ve witnessed these founders endure a rollercoaster entrepreneurial journey, braving challenges like Covid and equity winters, and, of course, embracing triumphs.

Now, we are thrilled to present our Founder’s Playbook series, a collection of curated insights and experiences gathered from these remarkable founders. This series serves as a treasure trove of wisdom, where seasoned entrepreneurs share their valuable knowledge and hard-earned lessons with the startup community.

Whether you are a budding entrepreneur navigating the early stages of your venture or an experienced founder seeking guidance in uncharted territories, our Founder’s Playbook offers a reservoir of practical tips and inspiration to fuel your own journey. Embrace the knowledge shared within and join us in fostering a community of support and growth, as we continue to shape the future of entrepreneurship together. Do get in touch with us should you be interested to share your own war stories with the founder community.

Meet Niles Toh, the solo Founder who launched FoodRazor in 2015 as a SaaS business revolutionising F&B procurement and accounting processes. His first job fresh out of university was with a B2B SaaS company in 2014, managing regional sales and business development. It didn’t take long for Niles to see the potential of B2B SaaS as a profitable business model, sparking his desire to start his own venture. His father frequently shared his experiences dealing with inefficiencies in the F&B supply chain, which sparked the idea that this was an area where he could build a solution. Efficient ordering processes for ingredients are vital for a restaurant’s success as they directly impact the quality and consistency of the dishes served. By streamlining and digitizing this process, restaurants can optimise costs and reduce waste, while ensuring a delightful dining experience for their customers. This motivated Niles to start FoodRazor to address these issues.

Niles’ Journey in his own words

Being a solo founder came with its own trials and tribulations. One of the central challenges I grappled with was the limitations in my expertise and the sheer lack of bandwidth. In hindsight, I realized the immense value and strength that a co-founder could bring to the table.Initially, I had a co-founder, who unfortunately had to leave after a year due to personal financial concerns. As we were self-funding the business at that time, we couldn’t offer the stability he needed. This valuable lesson guided my approach when starting my current venture, SuperTomato, where I have the privilege of working alongside a dedicated co-founder.

Reflecting on my journey as a solo founder, I’ve identified some key aspects I would have done differently:

Seeking a Co-Founder from the Outset:I started with a co-founder who has the technical skillset that I am lacking. When bootstrapping a company, I think it’s more important to find a co-founder with both financial resources and time to commit to the long haul. The journey often takes more time than anticipated, so having someone dedicated to the process is vital.

Building a Strong Support Network: As a solo founder, the road can be isolating, and at times, overwhelming. In retrospect, I would have actively sought out and built a robust support network of mentors, advisors, and fellow entrepreneurs to share experiences, gain insights, and stay motivated.

Expanding beyond a Domestic Market: Initially, I thought we should concentrate on Singapore and establish a strong presence here before venturing abroad. However, I have come to realise that it would have been more beneficial for us to go global right from the start and allow our paying customers to direct us toward the most promising markets for expansion. Waiting for the perfect moment to be “ready” will only hold us back.

Methodical Fundraising Process:As a founder, it’s crucial to dedicate sufficient time and effort toward identifying suitable investors. This is particularly important for new entrepreneurs who lack working experience and require more guidance. It’s essential to identify an investor who can offer valuable advice and serve as a reliable sounding board, especially during the initial stages of your entrepreneurial journey.

I wish every Founder much success in their endeavours!

In June 2021 after six years at the helm, Niles made the difficult decision to exit FoodRazor. There was a buyer ready to take over the business and he recognized that he had reached a point of burnout and no longer felt he was the right person to lead the company.

Nonetheless, his unwavering passion for solving complex problems has been reignited after a much-needed break to re-energise himself. He has since embarked on his second startup, SuperTomato.ai, a hardware-focused venture which is already profitable. This time, Niles is joined by a co-founder who is a serial entrepreneur who has started multiple successful businesses. The presence of a co-founder has made a palpable difference, providing essential support and even sparking the inception of a third startup, MonsterBuilder.ai, which emerged from SuperTomato’s requirements.

Overall, Niles would summarise his mantra as “Think Big, Start Small, Go Fast!” and the startup journey, though challenging, is fulfilling and rewarding. Follow his journey on LinkedIn.

Reporting by Nicole Lim, Investment Analyst Intern, Class of 2023.

Once again, we were delighted to meet our investors, partners, and portfolio companies at our annual LP Day.

Held on 31 May 2023 at the magnificent Asian Civilisations Museum, we are grateful to guests who travelled from Hong Kong, Indonesia, Israel, Korea, Japan, Malaysia, Thailand, and USA to join us.

In addition to sharing the progress of our Fund, our guests were treated to an insightful programme:

Southeast Asia Investment Landscape by Mr Mike Imam, CEO, Silverhorn Group

INSEAD x GENESIS Venture Debt Report 2022/23 by Ms Alexandra von Stauffenberg, Associate Director, INSEAD

PANEL | Private Credit In A Post Silicon Valley Bank Era

Mr Or Alon, Vice-President, OurCrowd

Mr Tony Huang, Co-Founder & Managing Partner, K2 Venture Finance

Mr Andrew Tan, Chief Executive Officer, Asia Pacific, Muzinich&Co

Facilitated by: Dr Jeremy Loh, Managing Partner, Genesis Alternative Ventures

FIRESIDE CHAT | Leadership Lessons From Storms to Success with Mr Philip Yeo, Chairman, Economic Development Innovations Singapore Facilitated by: Dean Collins, Managing Partner, Dechert LLP

Facilitated by: Mr Eddy Ng, Partner, Genesis Alternative Ventures

The afternoon ended with cocktails and canapes between investors and founders, followed by a specially curated tour of the Asia Civilisations Museum’s world-class collection.

A special thanks to our LPs who shared their time expertise with our Founders so generously at our Founders’ Forum that same morning.

Relive the afternoon’s highlights with our Recap Reel:

SATURDAYS Expands Across Indonesia, Establishing Its Position as the Leading Eyewear Brand

New product lines, AI frame recommendation, and capital further accelerate growth

Jakarta, 10 April 2023 – Indonesian eyewear brand, SATURDAYS, continues to execute on its mission to provide access to affordable eyewear across Indonesia through tech-enabled omnichannel experiences. SATURDAYS has expanded sustainably its physical presence and will have more than 45 stores in 11 cities, including Jabodebatek, Bandung, Surabaya, Yogyakarta, Medan, Palembang, Makassar, Banjarmasin, Pontianak, Samarinda and Batam by the end of Q2 2023. The company has deepened its product offering by launching a kids’ collection and its more affordable VIBE series, starting at Rp395k (US$26). SATURDAYS also continues to provide fresh collaborations with well-regarded brands such as MARVEL, Indomie and key opinion leaders.

“Since we started SATURDAYS in 2016, our desire has always been to deliver exceptional value and customer experience to create an enduring brand. While the journey has been a roller coaster through the unprecedented COVID period, our focus remains the same; to build a sustainable business with strong fundamentals and healthy unit economics,” said SATURDAYS Co-founder Andrew Kandolha.

SATURDAYS recently opened its latest lifestyle store at one of the premier shopping destinations at Central Park Mall, Jakarta. The new store blends eyewear in a modern café that serves specialty Arabica coffee, teas and fresh baked artisan cookies from Naked Dough. Currently, SATURDAYS offer free drink for every eyewear purchase, and promo buy-1-free-1 drink for every returning customers by wearing SATURDAYS’ glasses to our stores.

“Naked Dough offers guilt-free and inclusive cookies, with less sweet options as well as gluten-free and vegan varieties. We are committed to providing a positive impact on our customers’ lives, without compromising on taste or quality,” said Naked Dough’s founder Jennifer Hermawan.

As part of its strategy to provide a seamless omnichannel experience, SATURDAYS continues to invest in technology providing convenience for customers to shop through website (www.saturdays.com), mobile app (Saturdays Lifestyle), chat, home and corporate try-on, or stores. The latest tech feature is SATURDAYS Artificial Intelligence (AI) technology, in which customers can scan their face and get customized recommendations on which frames are suitable for them, then try the frames on virtually instantly on their smartphone and finally order the pair(s) they love. SATURDAYS also provides wellness & employee benefits program for companies through cashless transaction or insurance providers. It has developed partnerships with 14 Third Party Administrator (TPA) and 23 insurances providers.

SATURDAYS recently secured venture debt funding from Genesis Alternative Ventures for an undisclosed amount to further fuel its expansion plan and solve the vision impairment problem in Indonesia. Previously, SATURDAYS received funding from local and regional venture capital firms Altara Ventures, DSG Consumer Partners, Alpha JWC, Kinesys Group and Alto Partners.

“We are excited to be partnering with SATURDAYS in their journey to digitize and democratize the eyewear industry. Under the stewardship of co-founders Andrew Kandolha and Rama Suparta, we believe SATURDAYS can become a disruptive eyewear brand who can deliver exceptional customer experience,” said Genesis’ Managing Partner, Dr Jeremy Loh.

About SATURDAYS

SATURDAYS is a tech enabled brand that offers designer quality yet affordable eyewear designed in house to fit and look great for Indonesian consumers. We provide omnichannel lifestyle shopping experiences through our app, website, home try-on and stores. We have grown to 45 stores in 11 cities across Indonesia as of April 2023.

At Naked Dough, we take great pride in creating the most delicious and high-quality cookies for our customers. Our commitment to using only the finest ingredients and refusing to take shortcuts is unwavering, ensuring that every batch of cookies is made with the utmost care and attention to detail. Our passion for creating the perfect cookie is reflected in every bite, making Naked Dough a go-to for cookie lovers everywhere.

About Genesis Alternative Ventures

Genesis Alternative Ventures is Southeast Asia’s leading private lender to venture and growth-stage companies funded by tier-one VCs. Genesis is founded by a team of venture lending pioneers who have backed some of Southeast Asia’s best loved companies. Armed with a strong reputation among entrepreneurs and investors, Genesis is a trusted partner in empowering corporate growth while minimising shareholders’ equity dilution. Genesis was founded by Ben J Benjamin, Dr Jeremy Loh, and Martin Tang in 2019.

The first quarter of 2023 was not pretty for the tech ecosystem globally – a continued venture capital reset, repeated rounds of tech layoffs, the failure of Silicon Valley Bank (SVB) and Signature Bank followed by the distressed sale of Credit Suisse, a near -60% decline in startup funding across all stages. The dreaded “C(ontagion)” word raised its ugly head in early March when the bank run on SVB came to light. With $175.4 billion in assets, serving an estimated 20,000 startups and 1,000 venture capital firms, and impacting the livelihoods of countless individuals, the stakes were high when the fate of SVB hung in the balance. The potential collapse of SVB, a historic and trusted financial institution for the startup ecosystem, caused widespread confusion and anxiety. As the go-to bank for founders and venture capital backers in Silicon Valley, SVB had long been regarded as the cornerstone of the financing universe for the tech industry. The unfolding events posed a grave danger that could potentially cripple the tech world, making timely resolution crucial for all those involved. So, just how important is SVB to Silicon Valley? At the end of 2022, SVB was the 16th largest bank in the United States and the largest by deposits in Silicon Valley, solidifying its position as the go-to bank for venture-backed tech startups. Legendary venture capitalist, Michael Moritz, a longtime partner at Sequoia Capital calls SVB “the most important business partner” in Silicon Valley over the past 40 years. According to Steve Papa, the founder and CEO of Parallel Wireless, a startup specialising in cellular communications systems, SVB’s collapse has left a significant void in the innovation economy that may take a decade for someone else to fill. As a serial entrepreneur with successive exits such as Endeca, an enterprise software company that was acquired by Oracle for $1 billion in 2011, and Toast, a restaurant-industry point-of-sale system developer that went public in 2021, Papa attests to the pivotal role SVB played in his startups’ success. SVB’s extensive network of venture investors, financing options, payment accounts for overseas customers, and other services were a driving force behind his ventures, underscoring the significant impact of SVB’s downfall on the startup ecosystem.

Lending Into the Tech Ecosystem Key to SVB’s Dominance as a Tech Bank

With over 40 years of experience, SVB has established itself as a key player in the Silicon Valley financing landscape through its venture debt offerings. Its comprehensive product suite, tailored to the unique needs of the tech industry, includes mortgages for executives, credit lines for VC funds to maintain capital flow, and venture debt for startups that may be considered uncreditworthy by larger lenders. Moreover, SVB’s global offices enable it to serve VCs and startups worldwide, extending its reach beyond the US where it has been a trusted banking partner for over half of all tech and life sciences startups.

As of December 31, 2022, SVB’s loan book was valued at $74 billion, encompassing a diverse portfolio of loans. Approximately 56% of its loan portfolio was dedicated to venture capital and private equity firms, secured by limited partner commitments and used for investments in private companies. Mortgages for high-net-worth individuals accounted for 14% of its loans, while 24% were allocated to technology and healthcare companies, including 9% for early and growth-stage startups. Notably, Bloomberg reports that SVB’s loan portfolio comprises primarily lower-risk and lower-yield loans and strong credit performance overall.

Genesis’ Jeremy Loh, who previously worked alongside SVB in a venture equity investor role during his time in the US, witnessed firsthand how SVB served as a supportive banker and venture lender to startups in their early stages. This approach created a sense of loyalty between founders and their capital backers. In fact, SVB’s wealth management arm, “SVB Private,” identifies potential private clients early on, providing liquidity for founders whose net worth is tied to their company’s valuation, particularly those who have exited their businesses and are flush with cash.

Credit Crisis or Opportunity post-SVB?

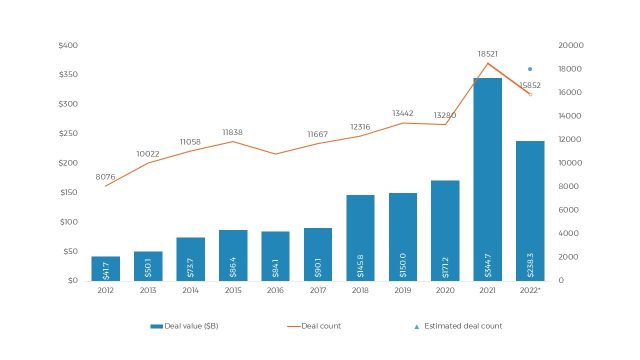

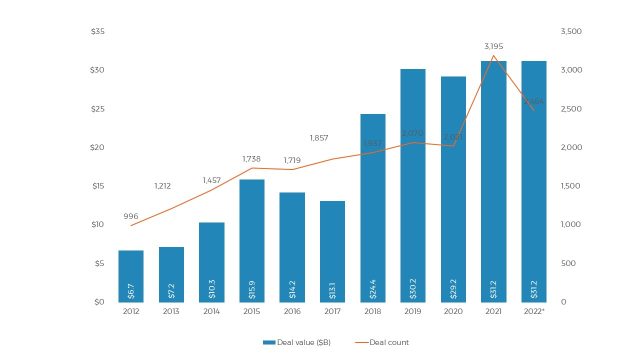

The surge in venture lending in recent years has been driven by startups’ increasing need to diversify their funding sources and reduce reliance on equity raises. PitchBook’s data shows that in the second quarter of 2022, the venture debt market saw the second-largest total value of loans in the past decade. Despite rising interest rates, over $30 billion in loans were provided to US-based VC-backed companies in 2022 (Figure 1), indicating a continued appetite for debt. SVB, being one of the largest venture lenders, exiting the market will create a gap for technology companies seeking to raise debt. It remains uncertain if other venture lenders will step forward to fill this void, especially for companies with undrawn SVB lines.

Figure 1: US venture debt activity – fourth consecutive year venture debt surpasses $30 billion in value. (Source: PitchBook)

So, who is stepping up to fill this gap left by SVB? In the US, First Citizens BancShares (Nasdaq: FCNCA) based in Raleigh has agreed to acquire SVB. This acquisition will position First Citizens as one of the top 15 banks in the US, and the 17 SVB branches will operate as “Silicon Valley Bank, a division of First Citizens Bank.” In Europe, HSBC has acquired SVB UK, which reported a profit before tax of £88 million for the financial year ending December 31, 2022. With this acquisition, HSBC aims to strengthen its commercial banking franchise and enhance its ability to serve innovative and fast-growing firms, including those in the technology and life science sectors, in the UK and internationally. This acquisition is part of HSBC’s ambition to become the tech bank of choice, as evidenced by its announcement in June 2019 to set up an $880 million technology fund to identify promising companies in southern China’s Greater Bay Area.

Reports indicate that former SVB employees have joined JPMorgan Chase, the largest bank in the US, in recent years, attempting to transplant their Silicon Valley network and investment expertise. During the SVB crisis, JPMorgan was seen as the biggest and safest bank in America by tech investors and entrepreneurs, and it is estimated that up to 90% of those who previously banked with SVB have since moved part or all of their accounts to JPMorgan, according to informal tallies shared by US VCs.

Additionally, there are existing US private credit players such as Hercules and TriplePoint, well-known names in growth and venture debt financing, that can potentially benefit from the SVB void to increase their market dominance. Hercules, with a track record of 18 years in venture and growth stage lending, has committed over $16 billion in capital to venture and institutionally-backed growth companies. Similarly, TriplePoint, an experienced venture lender, has overseen more than $9 billion in leases and loans to over 3,000 leading venture capital-backed companies.

With the increasing demand for venture debt, the venture debt market has become more lender-friendly. Overall, rates have risen and spreads have widened, allowing lenders to negotiate better covenants, and warrants have returned to debt term sheets as well. In the past, some lenders held back from warrants when company valuations were inflated and investors competed fiercely for deals, but the circumstances have changed. Lenders now see opportunities in recapitalization rounds, where having new equity is advantageous, and penny warrants do matter due to the longer timespan.

However, the repercussions of SVB’s decline could result in higher capital costs and tighter cash flows for startups, particularly those based in the US that have relied on SVB’s credit lifeline. As the largest and one of the most experienced venture debt lenders offering attractive rates to startups, it remains to be seen if the likes of First Citizen Bank and HSBC, or even JP Morgan can rise to the occasion.

In fact, recent insights from the Venture Debt Conference (March 2023, New York) via Pitchbook (reproduced below) confirm that while there have been no fundamental shifts where venture debt is concerned, the continued liquidity crunch coupled with the increased demand for venture debt will impact positively lending terms amidst a more realistic fundraising environment.

The use of venture debt has gained in popularity as many startups look to remain private longer and seek creative forms of financing that minimize dilution.

The collapse of SVB highlighted the importance of liquidity and the need to have cash on hand.

A frozen exit environment observed since the start of 2022, along with cooling fundraising figures, has created a liquidity crunch in private markets. This liquidity crunch and the exit of SVB creates a unique opportunity for smaller private credit players to take up market share.

Increasing levels of capital demand relative to supply will allow venture debt lenders to increase debt pricing.

While credit underwriting has not changed much fundamentally, shifting valuation paradigms will renew the importance of taking a hard, realistic look at growth and profitability outlooks.

Impact of SVB’s Collapse on Venture Debt in Asia

Over the last decade, there were two major forays into India and China as SVB sought to expand its overseas footprint. In 2008, SVB formally launched a venture lending operation after having opened offices in Bangalore in 2004 and Mumbai in 2007. However, 7 years later, SVB sold its venture debt arm to Singapore’s Temasek who renamed the entity Innoven Capital India, part of the Innoven Capital Group.

While SVB retreated from India, it subsequently set up a joint venture in China with Shanghai Pudong Development Bank. SPD-SVB was launched in 2012 to help Chinese startups do cross-border business with the US and facilitate capital raising across both shores. This JV was jointly owned by both banks but operating with its independent balance sheet. It is reported that SPD is now considering acquiring the SVB subsidiary in China.

In Southeast Asia, while market talk was that SVB was keen to understand the venture debt landscape in the region, no concrete expansion or lending took-off here. Taking a leaf out of its China and India expansion challenges, SVB perhaps recognized that it might have been a relatively large undertaking for it to attempt to build an organic venture debt business in Southeast Asia and instead chose to mostly co-lend with reputable venture lenders active in the region.

Given its lack of presence in the region, SVB’s collapse has not had a significant impact in Asia as Asian start-ups did not have any real direct exposure to SVB. On the flip side, the collapse did spur many parties to reconsider their corporate and personal banking relationships. At its 1Q’2023 AGM, DBS CEO Piyush Gupta mentioned that Singapore’s largest bank has benefited from inflows amounting to a “few hundred million” in the aftermath of the collapse of SVB given the perception that DBS and Singapore were perceived to be “safer” banking havens.

Startup valuations are also retreating with mid to late-stage companies facing mounting pressure to justify high valuations while seed-stage deals have seen valuation moderately increase. ‘Tourist’ investors who joined the flurry of VC investing and injected capital into startups at eye-popping valuations are taking a more cautious view of deploying more capital into this sector.

The recent funding trend should not be used as a yardstick to measure the demand for innovative solutions to the world’s pressing challenges. Technology remains critical in addressing issues such as climate change, financial inequality, aging populations, and healthcare, which are projected to worsen in the coming years. As a result, sustained investment in innovative technologies is essential. Long-term venture investors with multiple funds can breathe a sigh of relief, knowing that the demand for their expertise and resources will remain high in addressing these challenges.

Going forward, startups will also need to recalibrate expectations. The liquidity crunch will add another layer of difficulty for venture-backed startups looking to raise equity rounds amid the ongoing macroeconomic headwinds. The days of limitless capital to fund “growth-at-all-cost” are no longer there. Venture investors are actively seeking out startups that can demonstrate profitability, and startups must adjust their strategies accordingly. Today’s startup pitches highlight a low burn with a long cash runway – redefining the metrics of an attractive startup to a venture investor.

The House View is reproduced from Genesis’ Limited Partners Quarterly Update. The content in this article is meant to be informative and for general purposes only. It is not and shall not be construed as investment advice.