An article written by Gabriel Li (Vice President, Legal at Kredivo Group Limited) and Dr Jeremy Loh (Genesis Alternative Ventures) explains liquidation preference. Published by the Singapore Law Watch.

If you’re in the process of seeking equity financing or have done so previously, you’ve likely encountered the concept of “liquidation preference.” While online searches yield numerous articles providing a general overview, they often lack region-specific insights, particularly for founders seeking funding for a Singapore private limited company. This article offers a comprehensive introduction to “liquidation preference” within the Southeast Asia context, along with practical negotiation advice.

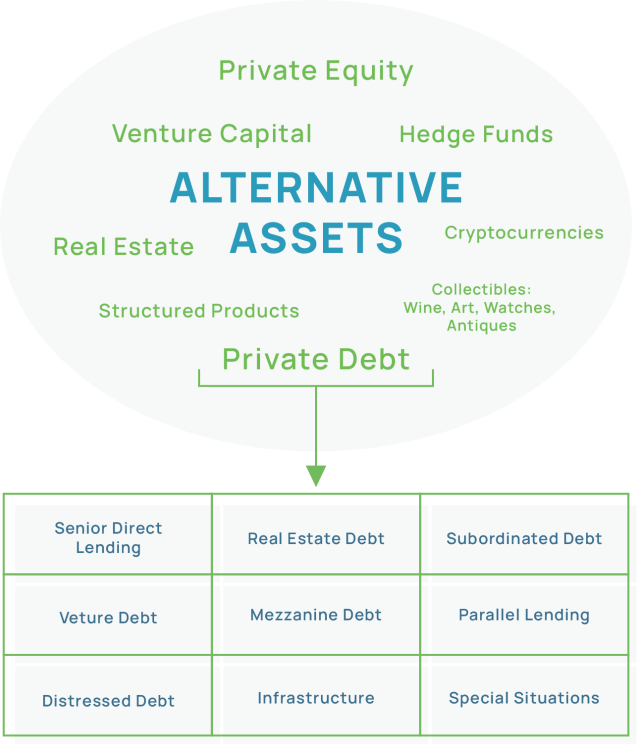

Private Debt has been grabbing headlines, with terms like Private Credit, Venture Debt, and Growth Debt often used interchangeably. However, it’s crucial to grasp the distinctions and understand the nuances. In this article, we unravel the intricacies of the overarching term “Private Debt” and focus on two key verticals – Venture Debt and Growth Debt – which are valuable financing tools for startups and scale-ups respectively.

Private Debt, a form of Alternative Assets, encompasses debt financing provided by private markets to companies outside traditional bank lending. Players in this arena include Debt Funds, Hedge Funds, Family Offices, Sovereign Wealth Funds, Non-Bank Financial Institutions, and Crowdfunding Platforms.

Venture Debt: Empowering Tech Innovators

Venture Debt is tailored for early-stage tech or tech-enabled companies (Series A and beyond). These companies, usually less than three years old, show high revenue growth, and have a unique/disruptive business model but are still burning cash. Venture debt has been a common financing tool in Silicon Valley but is still relatively new in Asia. Since Genesis first launched our venture debt fund five years ago, VC-backed companies in Southeast Asia have become more sophisticated about using venture debt as part of their overall capital financing strategy,

Venture Debt Structures: The Nuts and Bolts

Venture Debt typically takes the form of a term loan with a tenor of up to 36 months, repaid through monthly Principal and Interest amortization. Borrowers can access 20-30% of their recent financing round or cash on the balance sheet.

Reasons to opt for Venture Debt:

Filling working capital gaps for tangible outcomes, such as buying goods or raw materials.

Diversifying funding sources and reducing the weighted average cost of capital.

Minimizing dilution of early investors and founders across successive fundraises.

When to avoid Venture Debt:

Filling in for shortfalls or failures in equity fundraising.

The remaining cash runway is short and no other funding is available.

Funding Research and Development without a clear path to a commercial outcome.

Growth Debt: Fueling Expansion for Tech Titans

Growth Debt goes beyond Venture Debt by offering larger cheque sizes to mid to late-stage tech companies with revenues ranging from $10 million to over $100 million. Unlike Venture Debt, Growth Debt is not solely dependent on equity fundraising events and may serve as a substitute for equity. Examples of Growth Debt are Genesis’ loan to a leading global spatial data company before their IPO, as well as to Indonesian fintech firm, Akulaku. In essence, growth debt is a financing tool customized for later-stage startups who are hyper-scaling and preparing for an exit event.

Reasons to opt for Growth Debt:

Consolidating debt across entities or jurisdictions.

Refinancing costly or small quantum debt to benefit from improved terms e.g. lower interest rates or upsized debt.

Financing final rounds leading to profitability or pre-IPO stages.

Substituting for equity, reducing dilution for founders and early shareholders.

Funding projects with robust cash flows supporting debt repayment solely based on internal cash generation.

Acquiring an M&A target.

Credit Underwriting for Growth Debt: A Quick Overview

The credit underwriting process for Growth Debt is intricate, focusing on the company’s existing leverage, ability to achieve growth targets, reach profitability, and navigate market dynamics. Lenders assess the company’s attractiveness as a buyout or refinancing target, considering potential challenges to the original business case.

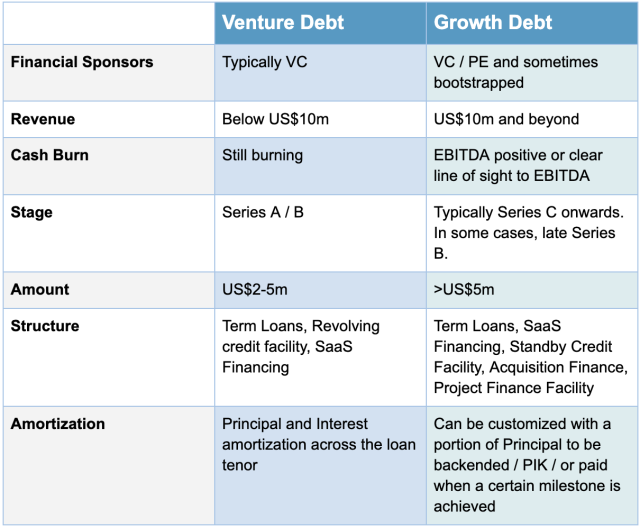

Comparing Venture Debt and Growth Debt: Key Distinctions

Venture Debt complements equity, emphasizing the fundamental quality of the borrower and its Financial Sponsors. Growth Debt at times may act as a substitute for equity, focusing on the company’s ability to execute growth plans independently and repay debt from internal cash generation.

The Genesis’ Approach: More Than Just Capital

Whether providing Venture Debt or Growth Debt solutions, Genesis takes a value-add approach, partnering with borrowers beyond cash. For insights on integrating debt into your fundraising plan or capital structure, we invite you to engage with us and explore the possibilities.

The table below outlines the differences and similarities between Venture and Growth debt.

For more information about Venture Debt and Growth Debt, please email us at contact@genesisventure.co.

An internship is a great way for undergraduates to gain real-world experience and develop new skills while still in university. However, getting an internship can be competitive, and the interview process can be daunting.

We asked our Communications and HR Manager, Michelle Low, to share some tips to help you ace your internship interview:

#1: Research, research, research

Before your interview, it is crucial to research the company you are applying to. This will help you understand their mission, values, and culture. Look at their website, social media accounts, and recent news articles to get a sense of what they do, who their customers are, and what their goals are.

You can also check employee reviews on websites like Glassdoor or better yet, reach out to their current and past interns for front-seat review. This will help you tailor your responses during the interview and show that you are genuinely interested in the company.

#2 Prepare for the predictable

Most internship interviews will include common questions such as “Tell me about yourself,” “What are your strengths and weaknesses?” and “Why do you want to intern with us?”

The best way to prepare responses to these questions is to understand yourself and what you can bring to the table. So list out your strengths (e.g. “advanced Excel skills” or “willingness to learn”) with examples of how you applied these strengths in other situations. It’s always best if your strengths match up to what’s stated in the job description.

In terms of areas of development, do not be shy about admitting them. In fact, the interviewer will appreciate your honesty and self-awareness. But always add what you are to mitigate your weaknesses. For example, “I am weak at proofreading my own work so I try to finish it ahead of time and ask someone to help me with proofreading.”

#3 Show enthusiasm and energy

During the interview, show your interviewer that you’re excited about the opportunity to intern with their company. Smile, make eye contact, and speak with energy and enthusiasm. This will demonstrate that you’re passionate about the work you’ll be doing and will help you stand out from other candidates.

#4 Ask thoughtful questions

At the end of your interview, you will likely be asked if you have any questions. Use this opportunity to ask thoughtful questions about the company, the internship program, or the interviewer’s experience. This will show that you have done your research and are genuinely interested in the company.

For instance, “I read on your website that venture debt is not the same as revenue-based financing but I am not clear as when startups should pick one over the other.”

#5 Dress for success

First impressions matter, even in online interviews. Dress appropriately for the company culture and industry. If you are unsure of the dress code, it’s better to be overdressed. Don’t forget to check your lighting, background, and internet stability.

#6 Follow up with a thank-you

Send a thank-you email within 24 hours of the interview, reiterating your interest in the internship and thanking the interviewer for their time. And don’t forget to attach any documents as PDFs – viruses are a big no-no.

With these tips, you’re sure to ace your internship interview and take the first step toward an exciting and fulfilling career. Good luck!

In a wide-ranging interview with Olivier Raussin, Co-Founder and Managing Partner of FEBE Ventures, we explore his career and experience working in the Southeast Asian tech ecosystem.

Olivier talks about his career in big tech, his own startups, and how he found his passion for venture capital. He shares insights into the challenges faced by startups and his thoughts on exciting trends in Southeast Asia, the future of venture capital, and offers advice for young professionals considering a career in VC

FEBE Ventures (“For Entrepreneurs, By Entrepreneurs”) is an early-stage Venture Capital fund supporting outstanding entrepreneurs in Southeast Asia.

Can you tell us how you ended up in Vietnam from France via Brazil?

I started my career in VC in Europe before having the opportunity to move to Brazil to lead the Latin American practice of my fund at the time, Project A Ventures. During the seven years I spent in Brazil, I had the privilege of working with many talented entrepreneurs and witnessing the incredible growth of the tech ecosystem there, including the emergence of several unicorns.

As I gained more experience investing in the region, I began to see many similarities between the tech landscapes in Latin America and Southeast Asia. Both regions have rapidly expanding economies (like Brazil, Mexico, Indonesia & Vietnam) that are ripe for digital transformation.

So, I decided to move to Singapore in order to immerse myself in the SEA startup scene and build relationships with entrepreneurs and investors in the region.

You pivoted a few times in your career. What prompted the move into VC?

I spent almost a decade of my career working in Big Tech, holding C-level positions at companies like Microsoft and Google in Europe. In between these stints, I had always felt an entrepreneurial itch and spent six years bootstrapping two startups.

However, it wasn’t until an old friend from university invited me to join his new $100M, operationally focused fund, that I realized that venture capital was a natural next step for my career. VC allowed me to combine my experience in Big Tech with my passion for entrepreneurship, and gave me the opportunity to work with talented entrepreneurs to help them build and grow innovative businesses.

You spoke about how startups don’t grow in a linear manner. Can you share with our readers about the wine business that nearly died many times but eventually did well.

When we were building an ecommerce business in Brazil, we faced many challenges that nearly brought us close to “be short cash” several times. These issues included a lack of capital, long working capital cycles. On top of that, we made mistakes in scaling too quickly and making the wrong hires. Through perseverance, we were able to turn it around. Today, the company is healthy.

This experience taught me important lessons about operating a business and gave me insights into the challenges that founders face. As a VC, I try to bring this empathy to my interactions with founders to help them overcome the hurdles that come their way.

How do you prioritize and manage your tasks and responsibilities on a daily basis?

In the morning, I spend time reading and working on mid-term strategic topics, as well as engaging in reflection and deep work.

My afternoons are reserved for calls and meetings. This is when I engage with founders to discuss potential investments and provide support to our portfolio companies.

Overall, I find it helpful to block out specific times of the day for certain types of work and prioritize my tasks based on their level of importance. This allows me to focus my energy on the most critical areas and maximize my productivity throughout the day.

What are some trends or developments in Southeast Asia that you find particularly exciting or interesting?

Among the trends that I find exciting in Southeast Asia, there are two in particular that I would like to highlight. The first is the emergence of Southeast Asia as a hub for SaaS startups that are building global solutions for the rest of the world.

Secondly, I’m impressed by the increased innovation and unique business models being developed in the region, as opposed to simply copying successful models from other markets. Startups in Southeast Asia are now leveraging their specific local and domain expertise to create businesses that are new and unique, which is great to see.

How do you see our industry evolving in the next 5-10 years, and how are you preparing for those changes

In the next 5-10 years, I see a few key trends emerging in the VC space. One is a consolidation of the various VCs & PEs in the ecosystem, which will likely result in the emergence of multi-stage platforms as well as ultra-niche plays (vertical, countries, technology) that cater to specific segments.

In addition, we will see the startup exit market maturing, with more opportunities for private equity exits.

How do you maintain a work-life balance and avoid burnout in a demanding and absorbing role?

I make sure to go for a run or go to the gym, practice yoga every day, and take my Golden Retriever, Samba, for a long walk once a day. I try to maintain a healthy diet by limiting sugar and carb intake. I also find it helpful to step away from work by disconnecting from Whatsapp and emails a few days a year to enjoy a full digital detox.

What advice do you have for young professionals who are considering a career in VC?

For those considering a career in VC, my advice is simple: join only if you truly love the work. This is not a job for those looking to climb the traditional career ladder of consulting or MBA programs. It requires a deep passion for technology, innovation, and entrepreneurship, as well as a willingness to work hard and commit for the long haul. VC is not a career with immediate rewards, and it can take years of hard work and persistence before seeing the fruits of your labor.

However, if you are willing to put in the time and effort, the rewards can be significant, both personally and professionally.

Finally, any advice for startup founders amid the current difficult macro-economic environment?

Growth-at-all-costs is over. Profitability is the new mantra. In today’s market, investors are looking for companies that can demonstrate a clear path to profitability and sustainable growth.

To achieve this, it’s important to be disciplined about controlling your burn rate and tracking your cash flow. This means being strategic about how you invest your resources, and being willing to make tough decisions when necessary.

In addition, investors like to see high margins, high repeatability, and high capital efficiency. These are key metrics that demonstrate a company’s ability to generate sustainable returns over the long term. On the other hand, we prefer to see low levels of capital expenditure and working capital.

The current environment is challenging for everyone, but with the right mindset and strategy, you can weather the storm and emerge stronger on the other side.

In 1983, Bill Biggerstaff and Robert Medearis, former Bank of America managers, founded Silicon Valley Bank to cater to the specific needs of startup companies. The banking industry at the time had little understanding of startups, particularly those without immediate revenue streams. SVB recognized this gap and developed loan structures that accounted for the unique challenges faced by these companies, managing risk based on their business models.

At the end of 2022, SVB was the 16th largest bank in the United States and the largest by deposits in Silicon Valley, solidifying its position as go-to bank for venture-backed tech startups. Legendary venture capitalist, Michael Moritz, longtime partner at Sequoia Capital calls SVB “the most important business partner” in Silicon Valley over the past 40 years.

What happened?

The collapse of SVB, a trusted banking partner and venture lender to many tech companies and known as the “bank for private equity”, was a sobering event. With over 40 years of experience, SVB had developed a comprehensive product suite tailored to the needs of the tech industry, offering mortgages to executives, credit lines to VC funds to keep capital flowing, and venture debt to startups that larger lenders deemed uncreditworthy. Its global offices enabled it to serve VCs and startups worldwide, not just in the US, where it was a banker for 50% of tech and life sciences startups.

However, the bank’s downfall resulted from a fundamental mistake: investing in longer-term mortgage securities with over 10 years to maturity, rather than shorter-term treasuries or mortgages. During a period of historic lows in interest rates, SVB invested depositors’ funds in long-term treasury bonds. And as the Federal Reserve raised interest rates to combat inflation, the value of those bonds plummeted, causing an asset/liability mismatch and leading to the bank’s collapse.

SVB with a loan book worth $74 billion as of December 31, 2022, had a diverse portfolio of loans. About 56% of its loan portfolio was dedicated to loans to venture capital and private equity firms, which were secured by their limited partner commitments and used to make investments in private companies. Mortgages to high-net-worth individuals accounted for 14% of its loans, while 24% were to technology and health care companies, including 9% to early and growth-stage startup companies. According to Bloomberg, SVB’s loan portfolio included many lower-risk and lower-yield loans. The bank’s non-performing loans in 2022 represented only 0.18% of its total loans, suggesting overall good credit performance.

So what happens now that SVB is no longer available to serve the startup community in the US?

SVB’s absence in the startup community in the US is likely to have significant consequences. While Silicon Valley Bridge Bank has stepped in as a temporary successor, encouraging its clients to diversify their deposits and operations between banks, it appears that the damage is already done and most of SVB’s clients have already withdrawn their funds and switched to larger banks.

VC and PE funds that relied on SVB’s subscription lines of credit to bridge capital calls will face challenges. These lines of credit allow General Partners of a fund to delay the funding commitment from their Limited Partners for up to a few months. These funds will now have to establish new banking relationships to channel their capital call funding, which could cause delays in funding new investments and have downstream impacts on startups that require funding.

The rise of venture lending in recent years has been fueled by startups’ need to diversify their funding sources and reduce reliance on equity raises. According to PitchBook data, the second quarter of 2022 saw the second-largest total venture debt value in the past decade.

In 2022, more than $30 billion in loans were provided to US-based VC-backed companies, which showed an appetite for debt despite rising interest rates. As one of the largest venture lenders, SVB’s exit will create a gap in the market for technology companies seeking to raise debt. It is unclear if other venture lenders will step forward to cover this gap, especially for companies with undrawn SVB lines.

The Venture Debt Outlook Going Forward

The consequence of SVB’s demise may include higher capital costs and tighter cash flows for startups, leading to more distressed companies. SVB, which has been the largest venture debt lender and has offered attractive rates to startups, may face challenges in the future as it is likely to be sold to another bank. This could potentially make it more difficult and expensive for startups to secure debt capital. While there are over 170 active venture debt funds in the US, according to PitchBook, these debt funds may need to step up to gain a bigger share of the venture loan market.

Chris first joined Genesis in June 2022 as an analyst intern for six months. Upon successful completion of his internship and graduation, he joined Genesis as a full-time investment analyst in January 2023.

We welcome Chris back and asked him a few questions about this experience so far.

Genesis [G]: Hi Chris, please tell us more about yourself.

Chris [C]: I possess a keen interest in finance, investments and entrepreneurship, and recently completed my Bachelor’s Degree in Business Management at Singapore Management University (SMU), majoring in Finance (Banking). My ultimate goal is to be an entrepreneur, starting a company and growing it whilst helping to improve the lives of others.

Outside of work, I am an avid basketball fan, watching the latest games or classic match-ups of the 1990s. I also enjoy football, golf, hanging out with friends, reading and watching movies, or trying out new experiences and challenges.

[G] At university, you majored in Finance. What prompted you to choose Finance?

[C] I’ve always been interested in Finance from a young age. I first started investing in stocks in secondary school, and I enjoyed figuring out the story behind the numbers, such as why did sales of a company improve, how would the macroeconomic environment affect the company, what is their value proposition against competitors, etc, and forming my own thesis based on the information gathered.

The diverse and dynamic nature of Finance was very engaging and exciting to me, allowing me to tap on different skill sets and see the interlink between business, finance and economics.

[G] Please describe your typical workday, if there is such a thing!

[C] There is no such thing as a typical workday! The amount of innovation out there is amazing, especially in the tech industry. It is dynamic and constantly evolving, and there is always something new to learn every day!

The fast-paced environment keeps me constantly engaged, while on slower days, I research emerging industries and technologies, or topics which I am particularly intrigued by, such as Artificial Intelligence (AI), Blockchain, Crypto, Metaverse, or Mixed Reality (XR).

[G]: What was your internship experience like at Genesis and what prompted you to accept the offer of a full-time analyst role?

[C] I initially joined Genesis with no experience in the venture debt/capital industry; however, the team was very open and willing to guide and mentor me.

Being an intern at Genesis is great, if you are inquisitive and enjoy working in a dynamic and fast-paced environment. As long as you take initiative and ask, the seniors, including the Partners, are more than willing to teach you.

Interns are also given the opportunity to take on more responsibilities, such as being involved in a deal from origination to execution, including attending networking events, talking to startup founders, analysing the deal and culminating with a presentation to the Investment Committee (IC) for approval.

Genesis places a strong emphasis on learning and development, whereby the team are ever-willing to share about their experiences, be it during weekly discussions or through masterclasses.

Besides working hard, the team knows how to have fun too! For our bonding day, we went for a short hike, raced each other in the Luge at Sentosa, and ended off with a durian buffet!

The dynamic and challenging nature of venture debt investing, coupled with the positive culture at Genesis and the opportunity to further develop myself prompted me to accept the conversion offer and continue my journey with Genesis as a full-time analyst.

[G]: Any memorable experiences at Genesis you’d like to share? What did you learn from it?

[C] One memorable experience would be that I was fortunate enough to be involved in a deal that went to the IC stage, whereby I analysed and presented it together with my senior, Josias Goh.

Throughout the process, we held many discussions with the Partners, and it was exciting to pick their brains and gain insights from the feedback given by them. Besides that, the Partners and the team were also very supportive, and constantly checked in with me and shared their experiences, or gave tips for my own personal development, which is testament to the positive learning environment at Genesis.

[G]: You shared about web3 and crypto during your internship interview. Can you tell us what sparked your interest in this area?

[C] I first came across Crypto when talking to my friends, and started dabbling in it just for the fun of it.

As I researched further, I found the underlying Blockchain technology particularly intriguing, as it has many potential use cases which could help make our lives more convenient and productive. I was further piqued by Blockchain when I took a module in SMU called Financial Innovation, where I learnt more about how it works, and did a project on Stablecoins. Blockchain’s potential to change our lives truly fascinated me, and there is still so much more for me to learn about it!

The ambition of any startup was to become a unicorn. However, with the recent battering of the financial markets and the looming threat of a 2023 global recession, the pendulum of venture financing has swung from feast to famine.

Startups in Southeast Asia have not been spared from the “perfect storm”. Gone are the days when venture funding was readily available for “growth at all costs.” Instead, investors have been tightening their purse strings and prioritizing strong unit economics, sustainable growth, and conserving cash. Therefore it is not surprising that Founders are feeling anxious and looking for alternative sources of financing.

To explore the ecosystem’s perceptions of such an alternative financing instrument, venture debt, INSEAD GPEI collaborated with Genesis Alternative Ventures to survey founders, venture capital firms, and investors.

Genesis welcomes our latest Limited Partner, OurCrowd, is a global venture investing platform that empowers institutions and individuals to invest and engage in emerging companies. OurCrowd manages more than $1.9B in committed funds for its 300+ portfolio companies and venture funds.

We sat down with Jon Medved (JM), Founder & CEO of OurCrowd. John is a serial entrepreneur and investor, who has been named by the Washington Post as “one of Israel’s leading high tech venture capitalists” and by the New York Times among the “top 10 most influential Americans who have impacted Israel.

Q1: You’ve been in the startup industry for a very long time. What is it that excites you about the industry?

JM: Startups are the lifeblood of technological innovation and progress. Decades ago, Lockheed Martin invented Skunk Works, and Xerox created Xerox Park, where the brightest minds could dream up big ideas unhindered by stultifying corporate red tape.

Today, the smartest companies in the world – including all the tech giants – realize that the only way to bring innovation into their products is to scout for startups developing relevant tech, invest in them, and snap them up. Today’s entrepreneurs have become Rockstars who are often celebrated and admired. They are responsible for building the world’s largest companies who have completely transformed our lives. Startups are developing the tech we need for computing, communication, and commerce, not just for the tech industry alone, but to address the critical issues of our time: food production, healthcare, clean water, sustainable energy and much, much more.

As a venture capitalist, I have the privilege of enabling visionary founders and innovators by connecting them with the investors who can fuel their startups and transform their dreams into commercial reality. Our companies literally save lives, heal the sick, and provide fresh food, water and clean energy where it’s most needed. They protect critical infrastructure from cyber-attacks. They provide the digital tools that help businesses grow. They entertain and they create employment. And when they succeed, they repay their investors many times over. It’s the best job in the world.

Q2: OurCrowd is a well-known equity investor and you’ve now launched a venture debt strategy. Can you tell us your rationale? What has been the reaction from your investors and startups?

JM: OurCrowd’s mission was always to democratize access to private markets, so in that sense it’s just a natural continuation of our journey. This initiative also came at a perfect time. Demand for venture debt is at an all-time high as entrepreneurs and investors alike realize its critical importance in the market.

This new debt product serves us in two ways. It allows us to further support our portfolio companies by offering them non-dilutive financing, which is highly relevant given the decline in valuations and the desire to avoid serious dilution from a down round. It also expands our value proposition to our investors with a cash-generating facility that provides steady income and much shorter duration than the equity investments. We are getting great feedback from both portfolio companies and investors for adding this new asset class, as evidenced by the oversubscribed Genesis first close.

Q3: Why did you choose to partner with Genesis?

JM: We decided to partner with Genesis because of the Genesis team’s strong domain expertise, with 40 years of VD/VC/PE experience and $100m+ venture debt deals executed. They are probably the most experienced venture debt team in Southeast Asia. The team’s performance speaks for itself in the early results from Fund I.

Genesis also gives us access to a unique market opportunity. Venture debt is growing strongly across Southeast Asia and high-growth companies that raise venture debt typically do so concurrently with an equity fund raise. In 2021, a record $621B was invested into global startups with $25B injected into companies in Southeast Asia. This represents a 3x increase over equity raised in 2020.

OurCrowd also likes to invest alongside strong LPs, like the Fund I investors who also decided to invest in Fund II and include some of the strongest institutional investors in the region. Moreover, we know many of the key members of the funds management for many years, and not only like them and appreciate them as fine human beings, but we continually are amazed by their talent and high ethical standards. When a great team addresses a huge and fast-growing market opportunity at the right timing, this is a good time to invest.

Q4: Where do you see the venture capital industry, especially venture debt, going in the next 5 years in SEA and Israel?

JM: A typical benchmark used by research analysts is to estimate the total size of the venture debt market as a percentage of total venture capital invested during a given year. Estimates are that the venture debt market in SEA represents ~2-5% and in Israel ~5-10% compared to 15-20% in the US. These two markets achieved fundraising records in 2021. Israeli startups raised $25.4b, a 136% increase on the previous year, while SEA startups raised $25.7b, a 167% YOY increase. We believe that the record VC money raised in 2021, maturing of the market and strong demand for venture debt amid the current global slowdown will continue to be the main drivers pushing the growth of this market.

Q5: How and where can startups in SEA and Israel collaborate together?

JM: Startups are shrinking the world. Cross-cultural collaboration is essential for innovation, because it breaks boundaries of thinking and attitude. Just look at how many of the top tech executives in the US are immigrants. One of Israel’s great strengths that has helped make our tiny country a global tech powerhouse is the fact that our population comes from more than 100 different countries, creating a rich cultural diversity that expands knowledge and thinking. Every time an Israeli startup begins a collaboration with a partner or customer from another country, it adds to its experience and effectiveness.

We are now seeing the same phenomenon in our new relationship with the Gulf states following the signing of the Abraham Accords, where Emiratis and Israelis are bringing different and complementary skills and experience to bear on a wide variety of issues and creating something brand new and even more exciting. In the same way, collaboration between startups in SEA and Israel can only enrich everyone involved and expand their horizons. Israeli companies can benefit from SEA skills in scale up and manufacturing, SEA companies can benefit from Israeli R&D prowess and deep tech innovation.

Q6: What do you look for in a founder or founding team?

JM: OurCrowd vets hundreds of startups every month and chooses perhaps one or two percent to add to our platform. Our founders must display technological excellence, relevant experience, original proprietary technology, good management skills and commercial sensibility. It is very rare for one person to have all those skills, so we tend to invest in teams of founders whose skills and experience combine to create the right group to establish, lead and build a company with a potentially commercial product. Moreover, we want to work closely with our teams, so it helps to like them!

Q7: What are the challenges and opportunities that you are seeing in the tech industry?

JM: The world is in crisis. We need answers to the critical issues facing our planet and its people. Startups can create the technology we need to fix the world. Just look at BioNTech, a startup founded by Turkish immigrants in Germany that created the vaccine marketed by Pfizer. Startups that tinker with problems that no-one needs to solve will not survive. But founders who identify a real problem, develop a practical, commercial solution and find a way to market will continue to succeed.

Q8: Any advice to founders on weathering the current downturn?

JM: This market correction was almost mandatory if you look at the soaring valuations of the past few years. Founders can no longer expect to enjoy the soaring double-digit price/revenue ratios that we have seen. There is still a lot of venture capital waiting to be deployed, but investors will want to see realistic business models and more modest spending. Founders should trim costs, extend their runway, and turn to alternative financing like venture debt instead of dreaming of huge cash injections from selling off tiny parcels of equity at high valuations.

Q9: What is your favourite movie and why?

JM: It’s A Wonderful Life. No explanation necessary.

Q10: What’s next for you?

JM: I have the greatest job and the cutest grandchildren in the world. I’m staying right here with them in Jerusalem, the most beautiful city on Earth.

We get it. Running a startup is a crazy roller coaster ride. That is why it is important to find and bring the right VC partners on board with you. You will probably meet many before deciding on a core team. And it all starts with a convincing pitch that is engaging, clear and concise.

When I googled “how to pitch my startup”, I got more than 42 million hits. I am sure most of the advice offered is sound, if a little generic.

Having worked in the startup ecosystem in both Silicon Valley and Southeast Asia, I have noticed that there is a difference in the way founders here approach their pitch. I have noticed that Southeast Asian entrepreneurs tend to be more conservative in their pitch approach and more reluctant to talk about their achievements (and I include myself in this category). There are many cultural reasons for this but such reticence does not serve startup founders well, especially when making their pitches.

Over the years, my team at Genesis and I have attended multiple startup pitch sessions and have given my share of feedback and useful tips to help founders in Southeast Asia sharpen their pitch. Here’s a quick summary of those feedback:

Be clear about your ask

It is perfectly fine to be upfront about what you are looking for – be it mentorship advice or an investment. Many founders feel shy about talking about money so early in a discussion but trust me, it is helpful for the VC to know your objective from the start.

For instance, if you are looking for funding, you can start by saying, “Thank you for your time today. I am looking for $6m funding for a 10% share of my agri-tech company.”

Or, if you are looking for strategic partnerships, “Thank you for your time today. I am looking for partners in the agri-tech and/or logistics space who can add value to my business.” It is also reasonable to seek introductions to business contacts or possible advisors.

Be proud of your mission and credentials

Once I sat in on a pitch from an edutech company and it was only after 5 or 6 slides that she revealed that she is a geneticist. Immediately that became interesting to me. What is the connection between genetics and education?

Most founders tend to have business, finance or engineering backgrounds. So when someone with academic achievements and industry experience turns up to share why they are on this mission, it certainly catches the attention of an investor.

Likewise, for your mission. Whether you are solving a payment problem or moving 1 ton of ugly food per day, if you are not excited about your mission, no one else will be.

So do speak with positive energy and conviction. I know this is not natural for many of us in Southeast Asia but it is important to “infect” the VC with your enthusiasm.

Be humble when receiving feedback

This sounds contradictory to #2 but it makes sense. The VC industry is a small one, particularly in our region. One of the first questions that VCs ask themselves is “can I work with this entrepreneur over the next 3-4 years and help build this business?”

“VCs invest in people, not ideas or technology.” Most investors are placing a bet on the founder’s ability to successfully handle the multiple challenges of growing a startup. And founders who are unable to handle a couple of tough questions in a pitch are less likely to raise money from investors.

So treat the feedback as a gift. An hour that a VC set aside to listen to your pitch may not end up in an investment. But the feedback could bring fresh perspectives, new ideas and insights for your business or even how to improve your pitch.

Be concise with your elevator speech

It is always good to be prepared to talk about your startup concisely. You’ll never know when you’ll meet a potential investor.

We suggest an elevator speech along these lines:

Think BIG: What is the end goal (e.g. save 10 tons of ugly food per day)?

Start SMALL: What are the low hanging fruits that you are plucking today?

Move FAST: How are you going to scale?

Starting with your Big Idea allows you to plant a seed into the investor’s mind. And if you get interrupted and don’t get to the other two parts of your elevator speech, at least you’ve communicated your mission. This leads me to the final point.

Be jargon free

Most VCs are finance- or economics-trained. A few of us are engineers by training. Even fewer of us were medical professionals.

While we may have picked up terms like “NFT”, “Metaverse” or “DAO”, it helps if you use layman terms in your pitch. Try pitching to your family or friends first; if they can understand what your business is about, the likelihood of an investor understanding it would be higher.

The tech and venture market will have its up and down cycles. Whatever the climate, there will always be venture investors looking for the next unicorn or decacorn. When you get an hour of time with a VC or a partner, it is more important to be ready with your pitch. And be prepared to evolve that pitch deck. You will be fascinated when you see the 40th version compared to your first deck.

We wish you much success and hope that these tips are useful in helping you elevate your pitch and raising the next round of funds.

(A version of this article first appeared on LinkedIn on 21 July 2022.)

It has been an incredibly busy two months for us at Genesis Alternative Ventures, the current market volatility notwithstanding.

In April and May, we took advantage of the reopening of global borders to visit our investors, partners, and portfolio companies in Tokyo, Seoul, and Indonesia. In May, we hosted our General Partners Advisory Board and Limited Partners to share the progress of the Fund and to discuss the macro-economic investment outlook. It was refreshing to catch up with everyone face-to-face and to reaffirm the trust that we built via two years of virtual meetings.

All the discussions I had were enlightening, insightful and relevant in the current market uncertainties and I thank everyone for sharing your thoughts and time so generously. As one good deed deserves another, I thought it would be useful to sum up and share my takeaways that might help guide us through these turbulent times:

Growth of venture debt : Amid rising interest rates and increased market volatility, private debt tends to shine and venture debt providers across Southeast Asia, India and the US are reporting a surge in deals and a growing pipeline.

Cash is King: With tighter funding market environment and falling valuations, startups should look for opportunities to consolidate and acquire good assets to strengthen their position while cutting back on cash burn to focus on profitability and preserve cash runway

Keep Calm and Carry On: Venture investors have indicated continued support for existing companies and will allocate more capital to their portfolio, instead of hunting for new ones. However, with freshly minted Southeast Asia venture equity funds like Jungle Ventures Fund IV ($600m), East Ventures multistage $550m venture and growth fund, Mass Mutual Ventures Fund II ($300m), there is still ample liquidity for early-stage companies seeking entry ticket funding. However, founders are advised to sharpen their pencils as the days of funding back-of-envelope ideas are gone.

There ARE Alternatives to TINA (There Is No Alternative): Navigating a challenging environment, sophisticated investors are pivoting from traditional portfolios that were based on a mix of public equities and fixed income. Increasingly they are looking for an alternative bucket of private equity, venture debt, and real estate where opportunities for better yields than liquid assets, with lower volatility and less correlation to headline risk.

Next month, we hope to share some insights on Founders’ sentiments from a survey of the entrepreneur community. I thank you in advance to all those who have kindly agreed to be surveyed and share your thoughts with us.

Disclaimer: The content in this article is meant to be informative and for general purposes only. It is not and shall not be construed as investment advice.

(A version of this article first appeared on LinkedIn on 3 June 2022.)